Asymmetrical Reciprocity is Bangladesh’s Strategic Gamble in the New U.S. Trade Order

By

Bangladesh was not alone in reaching a trade agreement with the United States under what can only be described as asymmetrical reciprocity. The governing principle of the US-Bangladesh Reciprocal Trade Agreement is clear: access to the world’s largest single-country market is a privilege—earned by fully opening up one’s own market that was judged as highly restrictive. In exchange for scaling back the punitive 37% “reciprocal tariff” imposed in April 2025 to 19%, Bangladesh has committed to sweeping tariff elimination, regulatory adjustments, and expanded imports aimed at reducing the persistent U.S. trade deficit with Bangladesh

This was the culmination of a long journey of negotiations, mostly under wraps, due to a non-disclosure agreement (NDA). On April 2, 2025, President Trump declared a national emergency to address what he described as a “large and persistent US trade deficit” and invoked the International Emergency Economic Powers Act (IEEPA) of 1977 to impose a 10% minimum “reciprocal tariff” on nearly all other countries, effective April 5, 2025. US average effective tariffs rose from 2.5% to an estimated 27%, ranging from 10% to 125% (on China).

World trade has never been the same since. Uncertainty became the new normal. Following changes and negotiations with individual countries, effective tariff rate fell to 13% as of December 2025.

In an evolving scenario of country-by-country trade deals, Bangladesh, among many other countries, reached agreement that calls for opening up of its trade to US imports while its exports are subject to 19% tariffs except for apparel exports which enter duty-free to the extent they use US cotton or man-made fibre. Lacking any market power in its bilateral trade with US, Bangladesh appears to have conceded to demands for opening up – for the US—its own highly restrictive trade regime. In the end, it became clear that it was not enough to just eliminate tariffs on some 2500 products currently imported from US and subject to low tariffs (averaging about 26%). USTR was looking for full openness to turn around the persistent US-Bangladesh trade deficit. But negotiations were subject to a non-disclosure agreement (NDA) that forced the Bangladesh team not to make public the important conditionalities being negotiated. A careful review of the Agreement now reveals that it is essentially a reciprocal market-access bargain, contingent on Bangladesh meeting a long list of conditions on tariffs, regulations, labor, environment, and security cooperation. It is the price to pay for getting access to the largest single country market on this planet.

Bangladesh, among many other countries, reached agreement that calls for opening up of its trade to US imports while its exports are subject to 19% tariffs except for apparel exports which enter duty-free to the extent they use US cotton or man-made fibre.

To be fair to the negotiators, Bangladesh is not alone in this new scheme of things on the world market. Other countries, big and small, powerful and not so powerful, all appear to have lined up to reach deals of their own. It is an affront to the rules-based trade order but when everybody does it what can the emaciated WTO do except watch. The rules-based trading order, painstakingly built over 75 years, entered a new era of unilateralism.

The core strategy of US policy, as the world has now recognized, is to bring down its trade deficit. The approach taken is to reduce the deficit country-by-country, although it belies logic of international trade. Bangladesh, running a trade surplus with the US for long, about $6 billion in 2025, with exports of $8 billion (mostly garments) and imports of $2 billion, found itself in Washington’s crosshairs.

What Bangladesh Conceded—and What It Secured

Under the Agreement, Bangladesh will:

- Expand imports of U.S. agricultural products (cotton, wheat, soybean) and industrial goods (aircraft, LNG);

- Eliminate tariffs—some immediately, others phased out—across nearly the entire U.S. import spectrum, by 2035;

- Align policies on regulations, labor, environment, and security cooperation.

In return, Bangladeshi exports face a 19% U.S. tariff—except apparel made with U.S. cotton or man-made fiber, which qualifies for duty-free access.

This is conditional trade with asymmetrical reciprocity.

Failure to sign would likely have meant a reversion to the April 2025 reciprocal tariffs of 37%—a scenario Bangladesh could ill afford. In that sense, the deal represents risk management as much as trade diplomacy.

The most immediate economic implication of the deal stems from Bangladesh’s commitment to augment imports by expanding purchases of key U.S. agricultural products such as cotton, wheat, soya bean, and industrial products such as aircrafts and LNG, alongside sweeping tariff elimination – some immediate and some in phases – on almost the entire swath of products that originate or is likely to originate from the US. The Agreement binds Bangladesh to a scheduled duty-reduction framework, even as most Bangladeshi exports continue to face U.S. reciprocal tariff of 19 percent. This means Bangladesh does not automatically gain free entry; rather, it gains a conditional pathway to preserve competitiveness and avoid harsher reciprocal measures, provided it aligns its import regime and broader policies with US expectations.

The Tariff Reduction Framework: For Uncle Sam only

The most consequential element is Bangladesh’s binding commitment to phase out tariffs on U.S. imports to zero by 2035.

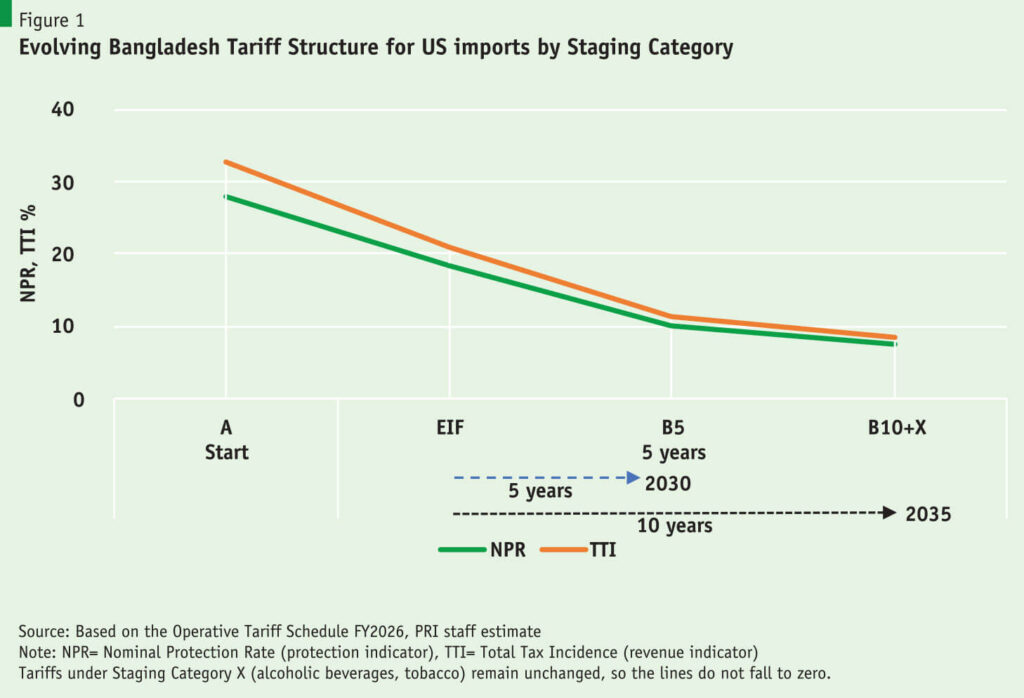

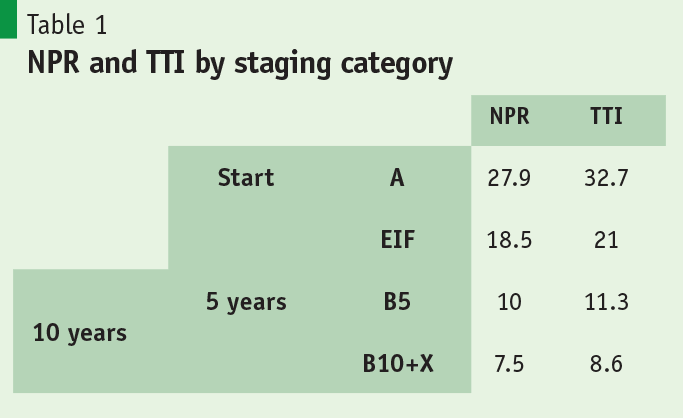

Elimination of tariffs – some instantly and others, in phases – is the one to watch. Bangladesh tariffs, already too high by international standards, must be phased out to zero by 2035 under this Agreement. Almost the entire swath of 7500 Bangladesh tariff lines will have to brought down to zero in about 10 years, with significant elimination at the very start of the Agreement. A tariff reduction framework is a key component of the Agreement (Schedule 1 of Annex), succinctly depicted in Table 1 and Fig. 1. A Staging Category framework has been formulated to cover the entire scheme over 10 years:

Staging Category (for US imports into Bangladesh) tells you when a tariff will be reduced or eliminated over time under this trade agreement.

A- (Immediate Elimination): Goods with this designation enter Bangladesh duty-free from the start. Actually, these have zero tariffs currently, so no issue there.

EIF- (Entry into Force): EIF implies immediate duty-free status, once the Agreement becomes active.

B5-(5-Year Phase-out): The product becomes entirely duty-free (0%) by January 1st of the 5th year.

B10- (10-Year Staging): Duties are reduced in 10 equal annual installments, becoming 0% on January 1 of the 10th year.

X (Exempt/No Change): MFN tariffs remain as is.

Fig.1 depicts the tariff-reduction scheme under the Agreement as tabulated in Table 1. Note that these estimates are exclusively for US imports, not on an MFN basis. Starting with an NPR of 27.9% in FY2026 (category A), the scaling down of NPR/TTI is depicted for the various phases, EIF, B5 and B10, showing that by 2035, all but the X items (mainly alcoholic beverages and tobacco) will be down to zero for US imports. The Agreement actually does not recognize anything other than customs duty (CD). Para-tariffs like RD, SD, AIT, AT are all assumed zero, except in the case of X category, which is left as is.

To summarize, of approximately 7,500 Bangladesh tariff lines:

- 422 lines (A category) are immediately duty-free (already zero-rated anyway).

- 4,500 lines (EIF) become duty-free upon entry into force.

- 1,538 lines (B5) phase out over five years.

- 672 lines (B10) phase out over ten years.

- 326 lines (X category)—primarily alcohol and tobacco—remain unchanged.

The US-Bangladesh trade agreement presupposes zero-tariff access to imports from US by the 10th year of the agreement (2035), with substantial front-loading of the tariff elimination done once the agreement becomes effective. The US offers zero-tariffs on mostly pharma and aircrafts (1638 tariff lines) but 19 percent tariffs on the rest, in addition to zero tariffs on apparel exports that use US cotton or man-made fibre (MMF).

Therefore, by 2035, virtually all U.S. imports—except Category X—will enter Bangladesh duty-free. This is, in substance, the core of what you have in a Free Trade Agreement. Yet the U.S. retains a 19% across-the-board tariff on most Bangladeshi exports. Reciprocity exists—but it is asymmetrical.

…by 2035, virtually all U.S. imports—except Category X—will enter Bangladesh duty-free. This is, in substance, the core of what you have in a Free Trade Agreement. Yet the U.S. retains a 19% across-the-board tariff on most Bangladeshi exports. Reciprocity exists—but it is asymmetrical.

The analytics emerging from the tariff reduction framework is tantalizing. First off, assuming Bangladesh applies special rates for US, the A category comprising 422 products/tariff lines are instantaneously zero-rated, as they already are in Bangladesh’s tariff schedule. This does not change the tariff structure at all as average NPR remains at 27.9% and TTI at 55.5%. The first salvo comes with EIF when the agreement becomes effective invoking zero-tariffs on 4500 products. NPR is down to 18.5% and TTI to 21%, a massive selective reduction in tariffs. The 5-to-10-year phase out further scales down tariffs so that NPR is down to 7.5% and TTI to 8.6%, all by 2035. Practically all imports from US are zero-rated by 2035. The X factor of 326 products leave tariff unchanged as if they are out of the Agreement.

Second, there is an implied “take it or leave it” signaling. Not signing it would have meant a return to US reciprocal tariff of 37% as imposed on 02 April 2025 – something Bangladesh (and possibly many others) can ill afford. Third, the question that comes to mind is whether Bangladesh can safely steer this bilateral agreement without ruffling feathers in other concessional treaties like EU’s EBA which has been a lifeline for Bangladesh exports for over 25 years. Fourth, though this Agreement scales back only tariffs on imports from US, as a special case, the non-disclosure agreement (NDA) forced negotiators to keep local stakeholders in the dark. (To my knowledge, similar NDA was applied to all other countries that sought a deal with the US).

The Strategic Opportunity: Cotton and RMG

The most promising feature of the Agreement lies in its interaction with the recently enacted Buy American Cotton Act 2025. Apparel made with U.S. cotton or U.S.-origin man-made fiber enters the U.S. duty-free.

Given that garments account for nearly 86% of Bangladesh’s exports to the U.S., this creates enormous potential. A significant share of RMG exports could now avoid the 19% tariff—provided sourcing shifts toward U.S. cotton or MMF. And that, to my understanding, is quite feasible.

Given that garments account for nearly 86% of Bangladesh’s exports to the U.S., this creates enormous potential. A significant share of RMG exports could now avoid the 19% tariff—provided sourcing shifts toward U.S. cotton or MMF. And that, to my understanding, is quite feasible.

Yes, U.S. cotton costs 4–6 cents per pound more than alternatives from West Africa and Asia. But:

- It is machine-picked, improving quality and reducing contamination;

- It enhances compliance and traceability;

- Most importantly, it carries a 19% tariff saving at the export stage.

The arithmetic could work in Bangladesh’s favor—if productivity improves and export volumes expand.

However, distributional tensions may arise. Textile producers (BTMA) supplying deemed exports to RMG firms must share in the gains. Coordinated policy engagement among BGMEA, BKMEA, and BTMA, mediated by the Government, will be critical.

The Political Economy Challenge

Bangladesh has lived under high protection for decades. The sudden erosion of tariff walls—even selectively for U.S. imports—could unsettle entrenched import-substituting industries.

Can domestic lobbies withstand competitive pressure from US imports? Can policymakers maintain coherence across EU EBA commitments and other trade arrangements? Can a selective zero-tariff regime avoid MFN complications?

These questions will confront the incoming government.

The NDA under which negotiations were conducted has left stakeholders with limited visibility into the full scope of commitments. Transparency will now be essential to sustain domestic consensus.

The new Government might be faced with questions from lobbyists in the domestic import substituting industry. Having lived for half a century on the back of high protection can they withstand a stampede of imports from US?

The Broader Implication: An FTA in Disguise?

A careful reading suggests that Bangladesh has offered the trade-liberalization architecture of a Free Trade Agreement—tariff elimination, regulatory alignment, labor and environmental commitments. Though investment does not appear in print there is already an existing bilateral framework called TICFA (Trade and Investment Cooperation Forum Agreement) that could be rejuvenated and aligned with this Agreement.

What remains incomplete is true reciprocity.

The 19% U.S. tariff hangs like a sword of Damocles. Trade diplomacy is not over; it has merely entered its next phase.

If this Reciprocal Trade Agreement deepens bilateral trade and strengthens strategic alignment, it could become a stepping stone toward a full-fledged U.S.–Bangladesh FTA—a milestone that has eluded Bangladesh for decades.

If this Reciprocal Trade Agreement deepens bilateral trade and strengthens strategic alignment, it could become a stepping stone toward a full-fledged U.S.–Bangladesh FTA—a milestone that has eluded Bangladesh for decades

History may record this Agreement not as capitulation, but as transition.

The real question is whether Bangladesh uses this moment to modernize and rationalize its overall tariff regime, strengthen competitiveness, and pivot from protection to productivity.

Trade policy for Bangladesh should not be just about market access but about economic transformation. Where Bangladesh economy stands today, a radical overhaul of trade policy is called for to lift Bangladesh to a higher growth trajectory where it really belongs.