Towards a Cashless Economy: A New Lifeline for Financial Inclusion

By

In a recent conversation at the Policy Research Institute, we asked a junior office assistant earning roughly USD 200 a month where he would turn for a loan to meet an urgent economic need. His response was stark. Formal retail banks were never an option; they do not exist in his economic reality. His choices were limited to high-interest borrowing from informal cooperatives or microfinance institutions; mechanisms that provide access, but often deepen vulnerability.

This is not an anecdote about individual exclusion. It is evidence of institutional failure and embedded financial exclusion. When a formally employed, salaried worker cannot access bank credit, the problem lies not in financial literacy or creditworthiness, but in the design of the financial system itself.

When a formally employed, salaried worker cannot access bank credit, the problem lies not in financial literacy or creditworthiness, but in the design of the financial system itself.

Almost as an afterthought, he showed his mobile phone. Based solely on transaction history, bKash had extended him a Tk 1,000 digital credit facility. The amount is small, but the signal is profound. A cashless platform, operating without branches, collateral, or paperwork, has recognized economic behavior that traditional banks have ignored. The issue is no longer whether digital finance can reach the underserved, but whether cashless economic transformation can receive the necessary public policy support to emerge as a new lifeline for financial inclusion.

Globally, the shift toward cashless economies is no longer a distant aspiration; it is an active policy choice shaped by technology, demographics, and development priorities. India’s Unified Payments Interface (UPI) now accounts for nearly 49% of all global real-time digital transactions, while mobile money platforms process over $4.6 billion in daily value worldwide. Brazil has pioneered branchless banking models through institutions like Nubank, which now serves over 80 million users, while Indonesia has leveraged digital platforms to scale nano-loans and expand access to credit for the underserved. Empirical evidence suggests such transitions not only enhance financial inclusion and reduce transaction costs but also contribute to economic formalization. For Bangladesh, the imperative is clear: a well-sequenced cashless transformation must be viewed not merely as a technological upgrade, but as a strategic lever for inclusive development. Done right, a cashless transition can be transformative. Done poorly, it risks deepening existing inequalities.

Bangladesh has made notable progress in few avenues of the cashless economic space. Mobile financial services (MFS), introduced in 2011 under a central bank-led regulatory framework, have fundamentally changed how people transfer money. More specifically, if the current monthly trend prevails, MFS will process transaction of around $120 billion annually reflecting both its scale and growth with around 90 million active accounts. What began as a tool for simple person-to-person (P2P) payments has evolved into a broader ecosystem supporting wages, remittances, government transfers, and merchant payments. With a nationwide agent network reaching deep into rural areas, digital finance has proven cheaper, faster, and less constrained by geography than traditional banking.

MFS will process transaction of around $120 billion annually reflecting both its scale and growth with around 90 million active accounts. What began as a tool for simple person-to-person (P2P) payments has evolved into a broader ecosystem supporting wages, remittances, government transfers, and merchant payments.

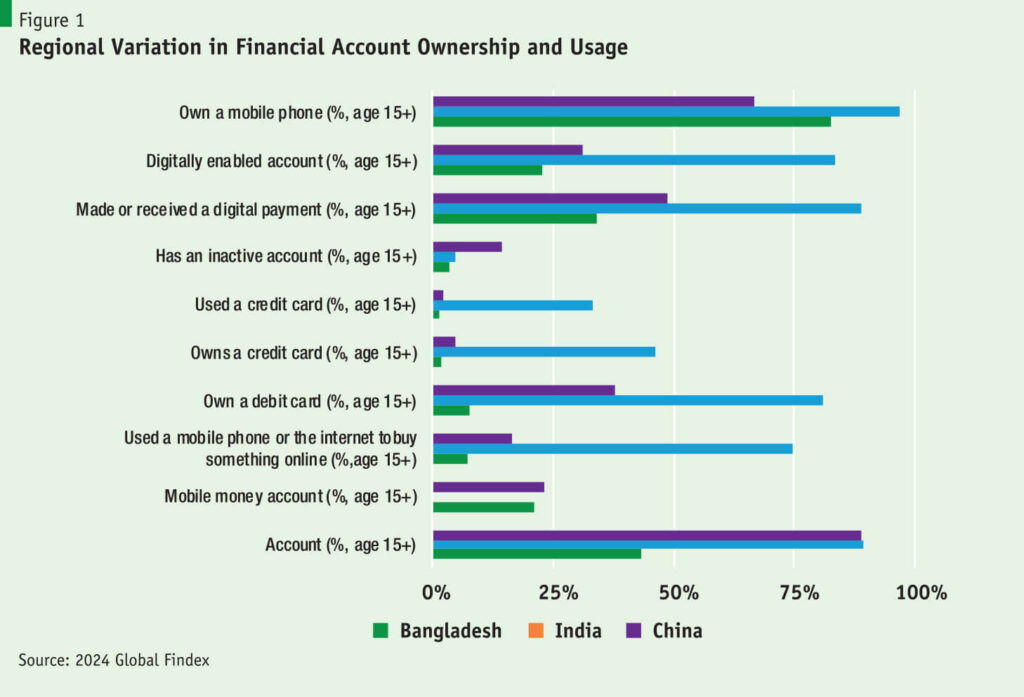

However, accomplishments on other notable avenues of the cashless space have been far limited. Bangladesh’s experience with QR-Code based transactions is far less impressive than countries such as Cambodia, Vietnam, India or China. Moreover, recent data underline both progress and enduring gaps. The 2024 Global Findex data for Bangladesh shows that only 43% of adults (age 15+) have a financial account, whether through a bank, another financial institution, or mobile money, indicating that a majority of the population remains outside the formal financial system. While 21% of adults hold a mobile money account and 23% have a digitally enabled account, nearly half the adult population remains outside the formal financial system altogether. Card ownership is particularly low: just 8% of adults have a debit card and only 2% a credit card, limiting the growth of card-based payments. By comparison, China and India project a much more impressive performance, demonstrating what is possible when infrastructure, regulation, and consumer trust align.

Off late, Bangladesh is also entering the age of digital banks and has started disbursing nano loans through mobile financial service, but these new instruments are still in their nascent stage – and is in need for public policy support to effectively deliver.

Nonetheless, in spite of the notable attainments and visible weakness within the cashless economic space, the dynamism and prospects only instill hope. For Bangladesh, moving toward a cashless economy is not simply about replacing banknotes with apps or payment cards. It is about unlocking financial inclusion, lowering transaction costs and strengthening economic governance, without leaving anyone behind. This is especially pertinent when traditional banking system has experienced significant expansion without promoting real financial inclusion.

For instance, our recent research for International Growth Centre (IGC) reveals that Bangladesh’s financial system remains highly unequal in its geographic reach and impact. Our findings uncover an uncomfortable truth: a mere 1.2% of loan accounts command over 75% of total lending in the country, reflecting an extreme concentration of credit access. Spatially, Dhaka and Chattogram dominate the system; holding approximately 65% of all deposits and 78% of total disbursed loans in 2024. These patterns are not merely the result of economic agglomeration; they point to a structurally skewed financial architecture that fails to intermediate capital effectively across Bangladesh’s geographic and economic peripheries.

In this specific context, microfinance has been traditionally seen as the fallback option to reach the unbanked or underbanked segment of the population, especially woman. Yet, its existing operating model has not fully replaced informal markets, nor can it meet the diverse financial needs of a growing, urbanizing economy.

Consequently, serious and carefully calibrated public policy commitment to the cashless economic transition agenda remains a critical tool for breaking free from the structural and traditional biases of the banking sector – ensuring that financial expansion coexists with real inclusion within the social and economic space. Yet, the risks of an uneven transition are real.

Large segments of the population – older people, rural communities, informal workers, and women – face barriers ranging from limited internet access and high device costs to low digital and financial literacy. Gender gaps are especially concerning: many women lack access to mobile phones or control over digital accounts, resulting in lower usage even where services are available. Furthermore, there are also institutional risks. Information asymmetries between financial providers and first-time users can leave consumers vulnerable to hidden fees, fraud, and misuse of data. Weak grievance redress mechanisms against frauds and gaps in oversight can quickly erode trust, undermining confidence in digital systems. In a prior study by PRI for Friedrich Naumann Foundation, it was found that one on ten MFS users face financial fraud. If these issues are not addressed, the move toward cashless transactions could end up reinforcing, rather than reducing, inequality.

A successful cashless transition, therefore, requires more than technological innovation. It demands coordinated public policy. Investment in nationwide digital infrastructure must be matched with efforts to ensure affordability, strengthen consumer protection, and expand financial literacy at scale. Regulation must strike a careful balance: encouraging competition and innovation while safeguarding stability and trust.

A successful cashless transition, therefore, requires more than technological innovation. It demands coordinated public policy. Investment in nationwide digital infrastructure must be matched with efforts to ensure affordability, strengthen consumer protection, and expand financial literacy at scale.

Most importantly, there must be a concentrated effort to ensure that the cashless financial ecosystem can harness Big Data from individuals, micro-entrepreneurs, small merchants, and low-income households to ensure that we move from traditional “physical collateral” to “information collateral” by creating a credible credit ratings ecosystem for the unbanked and underbanked population, so that digital banks and MFS can reach them effectively with their financial products.

On the whole, Bangladesh is at a pivotal moment in its financial evolution. While the infrastructure for digital finance is rapidly maturing, the trajectory of its cashless transition remains uncertain. A deliberate, inclusion-oriented approach is essential to ensure that digitalization does not entrench existing inequalities. A cashless economy is not merely the digitization of transactions: it is a reconfiguration of economic participation. If designed with equity at its core, it can democratize access to finance and enable shared prosperity. Without such intent, however, the shift risks becoming another uneven transformation that benefits the connected few and intensifying financial exclusion.

The authors can be reached at ashrahman83@gmail.com and samahjmajid@gmail.com.