Compilation of System of Environmental-Economic Accounting (SEEA): A Priority for Bangladesh

By

Introduction and Background

In a lecture delivered at the Washington DC ‘think tank’ Resources for the Future in 1992 (Solow, 1992, 1993)1, the Nobel laureate economist Robert Solow suggested that ‘an innovation in social accounting practice could contribute to more rational debate and perhaps more rational action in the economics of non-renewable resources and the approach to a sustainable economy’.

His suggestion emerged out of the consensus that the conventional System of National Accounts (SNA) followed in most countries a measure of the national income developed by the United Nations Statistical Division (UNSTAT), is not adequate for measuring or monitoring the impact of environmental changes on income or welfare. However, this conclusion was not surprising, since the development of the national accounting (mainly in the 1940s and 1950s) took place in a period where there was little concern on the impact of economic development on the environment. During that time, the conceptual basis and scope of the national accounts were governed by definitions of income and wealth which did not take into account the depletion of natural resources or the costs of environmental damage such as pollution.

There is now widespread realization that production and consumption activities have environmental consequences which impose considerable costs to the society, some of which would be borne by future generations. Therefore, there is a perceived requirement for information/data that will guide the sustainable management of the economic activity.

Following the above consensus or agreement there has been attempts to measure environmental impacts of the economic activities and to integrate these into the system of the SNA. Accordingly, 1993 version of the international System of National Accounts (SNA), published in 1993 by the United Nations Statistical Division (UN, 1993)2, addressed for the first time the possible incorporation of environmental costs and assets into the SNA. Instead of proposing a direct incorporation into the SNA, UNSTAT suggests adopting the concept of the ‘satellite’ account for compiling environmental accounts. The accounting formwork capturing the interaction between the economy and the environment has been formalized as the system of environment and economic account (SEEA). The SEEA began its development following the 1987 Bruntland Report, which was the first document to define sustainable development. SEEA has been adopted as international statistical standard by UN Statistical Commission in 2012. The SEEA focuses on (i) accounting adequately for the depletion of scarce natural resources and (ii) measuring the costs of environmental degradation and its prevention.

Currently, large numbers of countries have been implementing SEEA. A global assessment of SEEA was conducted in 2015 by the United Nations Statistics Division (UNSD) under the auspices of the United Nations Committee of Experts on Environmental-Economic Accounting (UNCEEA, 2015 3). The implementation of SEEAs may also increase manifold in near future due to its apparent use is SDG monitoring and evaluation. UN (2017 4) has shown that SEEA is at least linked to 9 SDGs out of the 17 SDGs.

Bangladesh considered a highly vulnerable nation to climate change and environmental changes. To confront the adverse impacts of the climate change, Bangladesh has already adopted the long term Delta plan. Implementation and monitoring of the Delta plan require coherent data on environment. SEEA is the most comprehensive accounting framework to capture environmental changes and its interaction with the economy. Despite the need, SEEA compilation has not been attempted in Bangladesh. This paper tries to suggest why and how Bangladesh may compile SSEA.

What is SEEA?

SEEA is a conceptual framework for measuring the interactions between the environment and the economy. SEEA is an outcome of the combined contributions by the United Nations, European Commission, Food and Agriculture Organization, Organisation for Economic Co-operation and Development, International Monetary Fund, and World Bank Group. It has been adopted as international statistical standard by UN Statistical Commission in 2012. Thus, SEEA is an internationally agreed statistical framework to measure environment and its interactions with the economy. The broad nature of SEEA suggests it is suitable for all countries and all aspects of environmental accounting. As mentioned above, SEEA is a satellite system of SNA and incorporates environmental and economic information together using SNA principles, concepts, and definitions. SEEA guides the measurement of: (i) the stocks of natural resources; (ii) their flows into and within the economy; and (iii) the flows of residuals back to the environment.

SEEA is a conceptual framework for measuring the interactions between the environment and the economy. SEEA is an outcome of the combined contributions by the United Nations, European Commission, Food and Agriculture Organization, Organisation for Economic Co-operation and Development, International Monetary Fund, and World Bank Group. It has been adopted as international statistical standard by UN Statistical Commission in 2012. Thus, SEEA is an internationally agreed statistical framework to measure environment and its interactions with the economy.

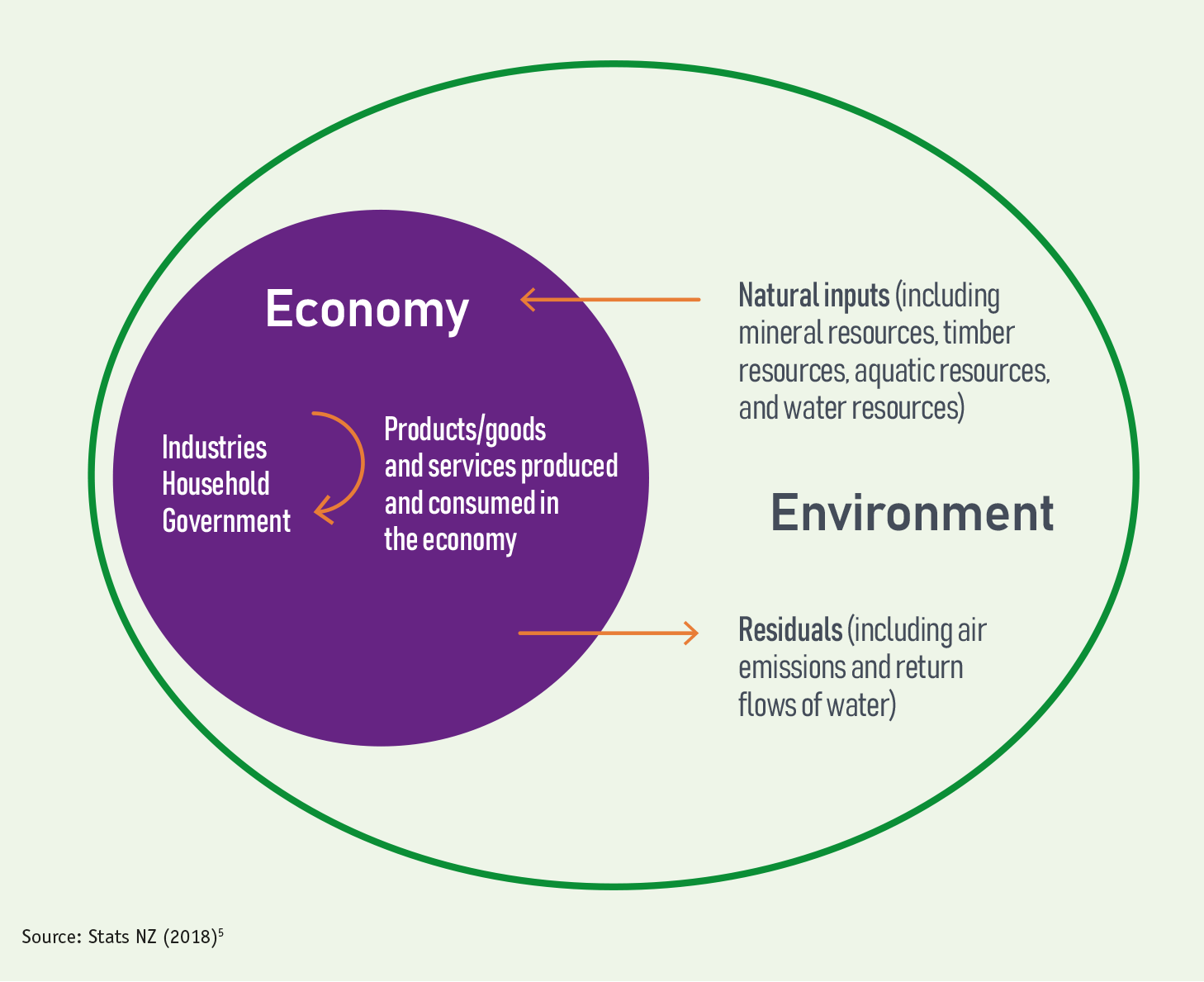

Adjacent chart captures the product flows within the SEEA structure. It measure the value and volume of many natural resources (through monetary and physical stock accounts). It also identify the industries using natural resources and the extent of emissions and discharges to the environment resulting from economic activity (through monetary and physical flow accounts). Moreover, measure the amount of economic activity undertaken for environmental purposes, such as expenditure on protection and management, and other transactions including taxes, subsidies, grants, and rent (through environmentally related economic transaction accounts).

Global Implementation of SEEA

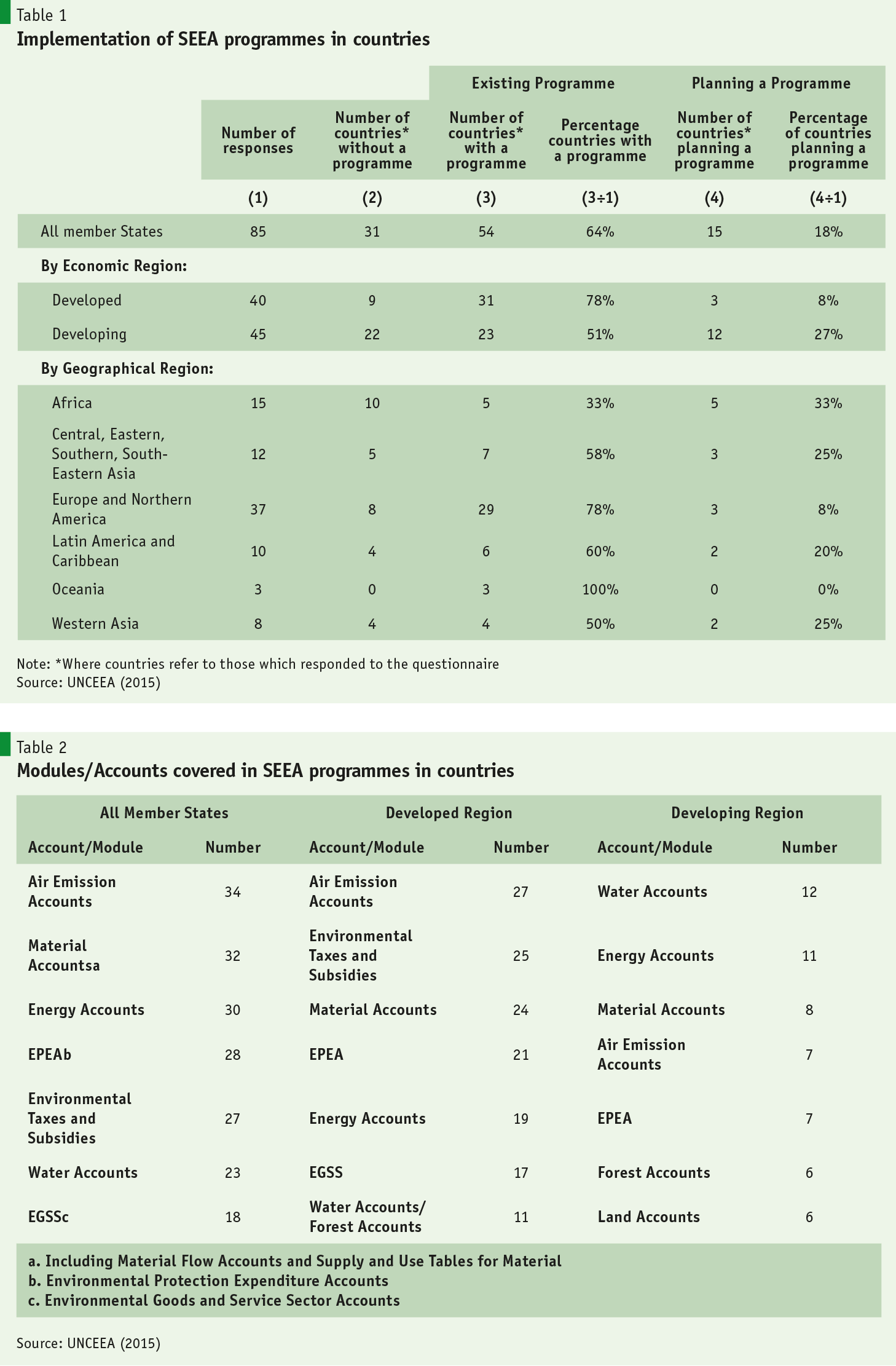

As mentioned above United Nations Committee of Experts on Environmental-Economic Accounting (UNCEEA) conducted a survey to understand progress in the implementation of SEEA among its member countries. The survey tool place in 2014. Earlier in 2006 a similar survey was commissioned. In 2014, the survey questionnaire was sent to 192 member countries – 85 countries responded implying a response rate of 44 per cent. The key observations are summarised below which may have implications for the design and implementation of SEEA in Bangladesh.

Out of the 85 countries, 54 of them are implementing SEEA implying an implementation rate of 64 per cent. Moreover, 15 countries (or 18 % of the sample) have been planning to implement SEEA. Developed countries have higher implement rates of 78 per cent compared to the 51 per cent implement rates for the developing countries.

SEEA implementing countries altogether have covered 192 modules/accounts with top three accounts covered by most countries are the ‘air emission’ accounts (in 34 countries), ‘material’ accounts (in 32 countries), and ‘energy’ accounts (in 30 countries). The module preferences are different in developed and developing countries. The top three modules in the developed countries are ‘air emission’ accounts (in 27 countries), ‘environment taxes and subsidies’ accounts (in 25 countries), and ‘material’ accounts (in 25 countries). The ‘water’ accounts (in 12 countries), ‘energy’ accounts (in 11 countries), and ‘material’ accounts (in 8 countries) are the top three modules/accounts in the developing countries.

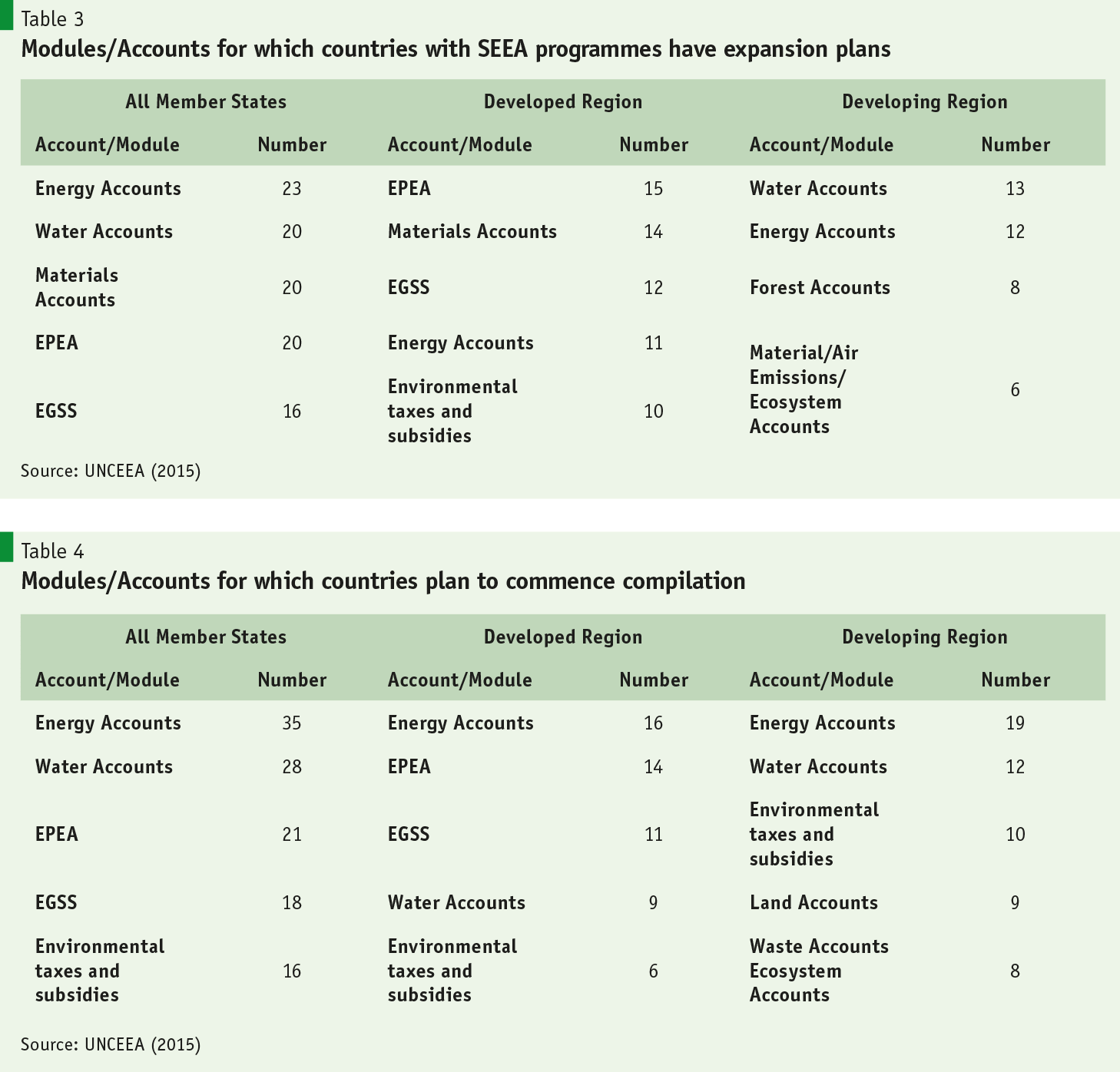

Table 3 present the five main accounts/modules for which countries with existing environment programmes intend to expand compilation. Although, the list of accounts/modules is largely the same as Table 2 for the developed region, results from the developing region suggest that, in addition to water and energy accounts, some countries are focussing expansion efforts on forest accounts.

Table 4 shows the modules for which countries have plans to begin compilation, disaggregated by economic region and the existence of a current programme. Overall, the top five accounts for which countries planned to begin compilation were energy accounts, water accounts, EPEA, EGSS accounts and environmental taxes and subsidies accounts.

Approaches to SEEA Compilation in Bangladesh

• Identification of Modules/Accounts: an important advantage of the SEEA compilation strategy is the flexibility with regard to choice modules/accounts for the country specific SEEA and as well as the selection of the underlying indicators defining the accounts. Following the trend of the emerging countries who are planning to begin compilation of SEEA intend to start with the ‘Water’ account, Bangladesh may start the SEEA implementation by first compiling the SEEA – water account. While compiling an account other auxiliary accounts such as ‘environment tax and subsidy’ may also be compiled. Similarly, for completeness the modules/accounts may also be linked to the SUT (supply and use table) and IOT (input-output table). Suggested SEEA accounts and their sequencing in Bangladesh may be : 1. Water Account and Transaction; 2. Energy Account and Transaction; 3. Mineral and Natural Resource Account and Transaction; and 4. Air Emission Account and Transaction.

• Formation of Technical Working Group: since compilation of SEEA is dependent on number of agencies and stakeholders, it important to form a technical working committee involving them.6 Institutional arrangements followed in other developing nations may also help Bangladesh to establish the technical working committee as well as their scope of interaction. Bangladesh may start with the key agencies (e.g. DOE, Ministries of Water, Industries, Land, Agriculture, and Research Institutions) with the option of inducting other agencies as and when required.

• Establishment of Data Collection Protocol: environment data are usually collected from businesses, private sectors and public sector organizations. However, environment data are not readily available. This is a common problem almost everywhere but more prevalent in developing countries like Bangladesh. Lack of environment data should not be surprising in the context of Bangladesh. Thus, Bangladesh will need to invest time and resources to collect data from various agencies. The key tasks will be to identify the sources (or agencies collecting the data), set up the data collection and sharing protocols and provide technical assistance to the data collecting agencies to improve data quality and frequency.

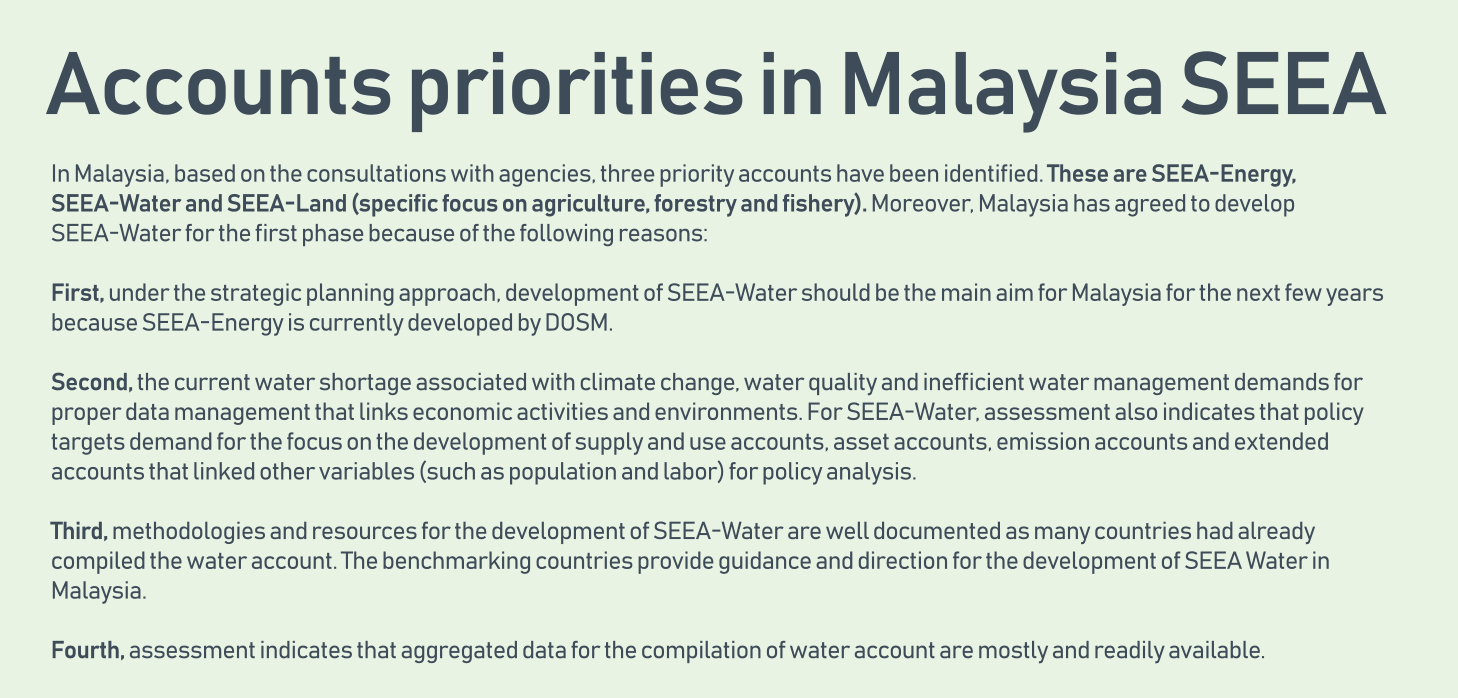

• Enhancement of Staff Capacity: almost all developing countries have been encountering problem of paucity of trained staff. Lack of human resource or trained staff may likely be identified as a key constraint to compile SEEA in Bangladesh. A needs assessment of staff should be carried out to identify knowledge gaps in specific areas. Thereafter, both in country and external training should be arranged to strengthen capacity of the BBS staff. In this context a strategy may be to seek technical assistance from Malaysia. Malaysia has compiled SEEA under a road map between 2016 and 2020. This will fall appropriately within the purview of the ‘South-South’ cooperation. Bangladesh may seek assistance in the areas of staff capacity development and knowledge sharing7.

• Adoption of a Phased Implementation: Bangladesh may adopt a phased approach to compile SEEA. It is envisaged a three phased approach over a five year period between July 2022 to 2026 (or January 2023 to 2027) to implement SEEA in Bangladesh.

Phase one will be a short-term planning and mobilisation phase for 5 months. This phase will focus on the formation of the setting and formalizing the governance structure, establishing the technical working committee, identification and agreement on the sequencing of modules/accounts and list of indicators, determining strategy to enhance staff capacity, formalization of the data collection protocols8, establishing data sharing and management, and promoting inter- and intra-agencies cooperation, and mobilising funding for the second phase.

• Second phase will be a twelve month-period phase. In this phase SEEA–water account will be compiled. This compilation will include physical stocks, and flows; monetary flows; transaction account – environmental expenditure, taxes and subsidies on water. In addition it may include incorporation of SEEA water accounts into existing SUT and IOT. It may be considered as a pilot phase and hence it would be compiled in two parts – part 1 may include structure, data collection, compilation and analysis; whereas part 2 may focus on dissemination, re-verification and finalisation.

• Third phase will cover three and half year. In this phase SEEA–energy, air emission and mineral and resource accounts will be compiled. In accordance with the design of the SEEA–water account, the compilation of all other accounts will also include physical stocks, and flows; monetary flows; transaction account – environmental expenditure, taxes and subsidies on energy, air and resources.

Conclusion

• Development of SEEA account in Bangladesh will allow systematic collection and compilation of environment data/statistics following globally accepted guidelines. If compiled appropriately SEEA will provide a comprehensive framework to track the state of natural resources in Bangladesh (e.g. forest, land, water, and fisheries etc.) and as well as the extent of flows of residuals discharged into the Bangladesh’s environment through the production and consumption of goods and services.

• Similar to the treatment of economywide data sets (e.g. Supply and use table [(SUT), input-output table (IOT) and social accounting matrix (SAM)], SEEA data can be combined with the various modeling techniques to analyse the implication of public policy (government expenditure and investment) on the economy and environment. Recently, the computable general equilibrium (CGE) model has been extended to link with SEEA to construct analytical tools known as Integrated Economic-Environmental Modelling (IEEM) platform. IEEM helps analysis of public policy and investment impacts on the economy and the environment in a quantitative, comprehensive and consistent framework (Banerjee, Cicowiez, Horridge, and Vargas, 2016)9.

• The outcomes of SEEA/SAM/CGE models can be used to prepare the benefit-cost analyses to assess the merits and demerits of various (and alternative public policies) for sustainable development in Bangladesh. For instance, outcomes of SEEA powered benefit cost analyses would help policy makers to decide on the introduction of carbon tax, installing renewable energy to replace fossil fuel energy, coal based transportation versus gas based transportation etc.