Raising Re venues and Empowering Bangladesh’s Cities Through Property Tax Reform

By

I. Bangladesh Property Taxes: Dramatic Under-Performance and Potential

Bangladesh is a revenue-starved country. Its tax-to-GDP ratio of 7.5% places it in the bottom decile of countries globally. Given its lower-middle-income status, tax revenue as a share of GDP should be more than twice that, making it comparable to India, which has a tax-GDP ratio of around 18%. This shortfall means critical public services in education, health, and infrastructure go unfunded, trapping the economy on a low-growth, poverty-reduction path.

The revenue situation is five times worse for property taxes, or ‘holding taxes,’ as they are locally termed. Bangladesh collects property taxes of only about 0.03% of GDP, compared with an average of 0.4 to 0.5% for lower-middle-income countries or the target of 1% of GDP for 2036 set in the National Task Force on Tax Reform’s (NTFTR) comprehensive report, A Reform Agenda for Restructuring the Tax System (NTFTR, 2026).

The silver lining is that the gap between potential and actual collections indicates the enormous revenue that remains untapped for financing public services and urban development. This article makes the case for property tax reform, lays out the implementation pathway, and touches on the political economy considerations that any serious reforms must confront.

The article proceeds as follows. Section II explains why property taxes are important. Section III draws on international experience to establish how far behind Bangladesh stands and what the revenue potential looks like. Section IV diagnoses why the current system fails so comprehensively. Section V outlines the reform strategy and its four pillars. Section VI addresses the political economy of compliance. Section VII concludes.

II. Why Are Property Taxes Important?

Property taxes are important, first and foremost, because Bangladesh desperately needs revenue, and they represent enormous, untapped potential. The National Task Force on Tax Reform has produced a comprehensive road map for national tax policy reform. Property taxes are an integral part of that agenda and represent an opportunity to raise revenues by up to 1% of GDP over the medium term.

Second, property taxes can specifically finance the cities and towns of Bangladesh. At present, Bangladeshi cities suffer from severely inadequate infrastructure and public services, leading to chronic traffic congestion, pollution, unsanitary waste disposal, and widespread waterlogging. Health and education outcomes in most urban districts are, paradoxically, worse than in rural areas. Industry is migrating to rural corridors, and employment growth in urban areas has sharply contracted. Because most future growth must take place in cities, their fiscal starvation becomes a national development problem. Property taxes address this in two ways: they provide the revenues needed to deliver public services to the 40 to 50% of the population already living in urban or semi-urban areas; and, properly designed, they make city governments accountable to their populations.

Last but not least, property tax is a powerful instrument for addressing the sharply rising inequality in Bangladesh’s development. At present, low property tax collections effectively amount to a massive subsidy for upper-middle-class and wealthy property owners. Wealth taxes face formidable implementation challenges and adverse efficiency impacts. Urban land values in Dhaka have grown at roughly 3.6 times the rate of income growth since 1995; a capital value-based tax would capture that appreciation directly, rather than relying on the hopelessly under-reported rental values that the current system tries and fails to tax.

III. Lessons from International Experience and Bangladesh’s Property Tax Potential

Although every country’s context is distinct, the challenges of property tax collection are, from an economic standpoint, unsurprisingly similar across countries at comparable levels of development — and, encouragingly, so are the solutions.

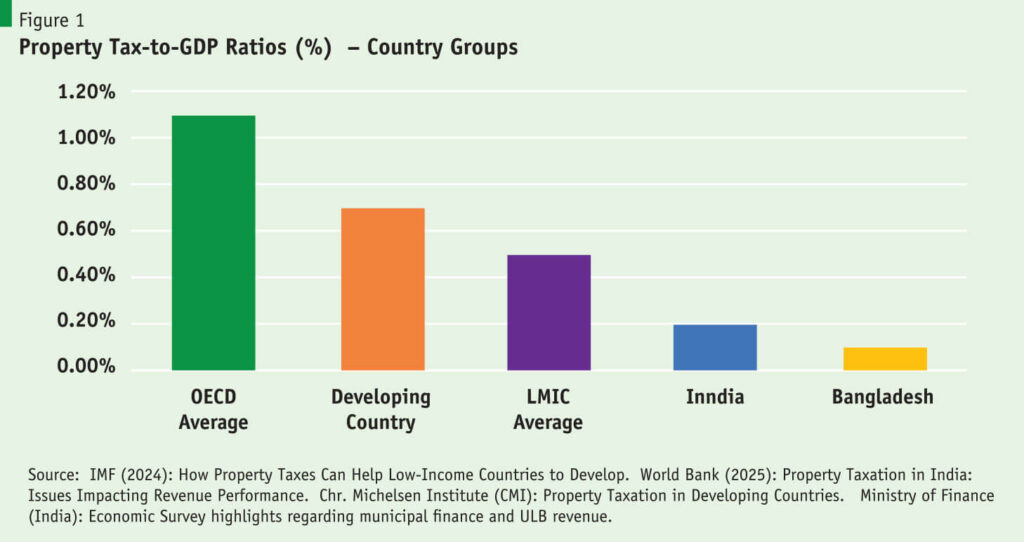

The first striking finding is how dramatically Bangladesh lags behind its peers. As a share of national GDP, Bangladesh collects roughly 0.1% in property and holding taxes — about one-fifth the rate of comparable lower-middle-income countries, one-seventh that of all developing countries, and less than one-tenth the rate of OECD economies. Even within India, which presents a generally poor picture, there is a wide disparity: Maharashtra and the southern states of Karnataka and Tamil Nadu each collect between 0.25 and 0.35% of state GDP in property taxes.

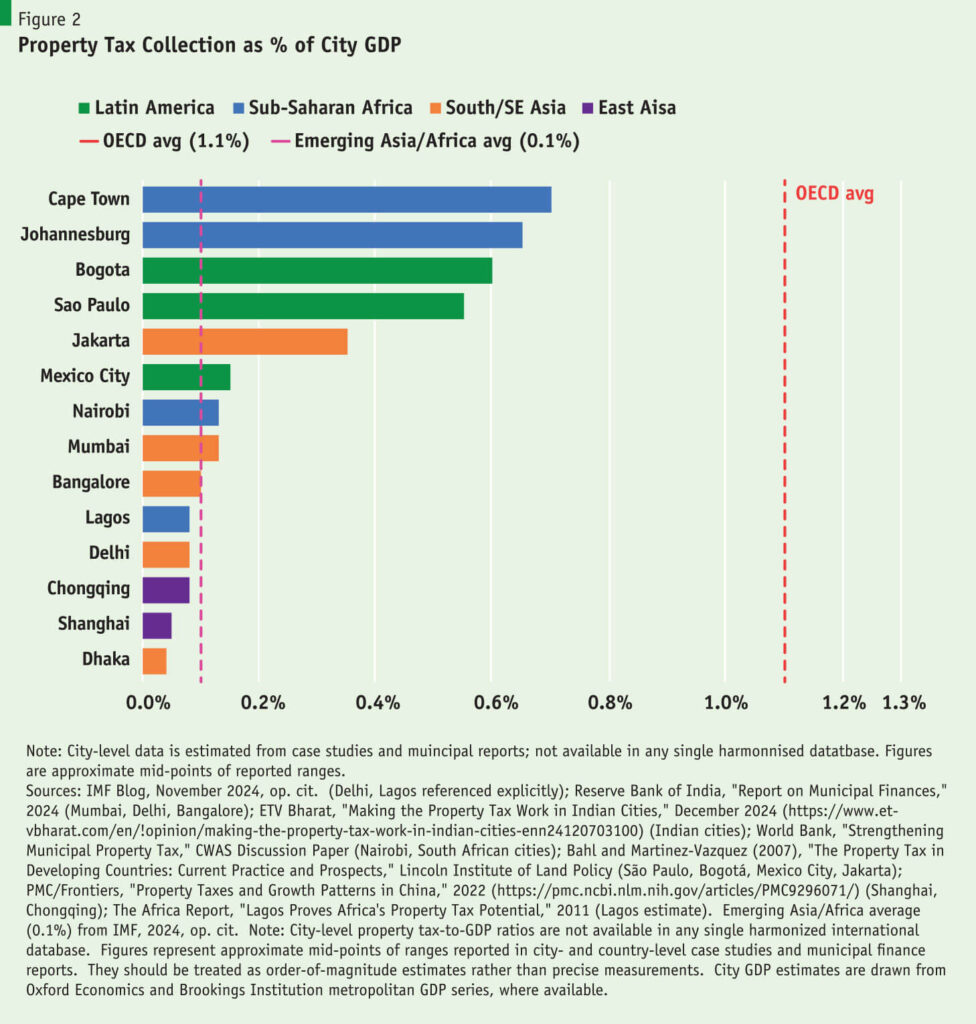

Bangladesh’s underperformance is even more striking at the city level. Figure 2 presents property tax collection as a share of metropolitan GDP across a range of developing-country cities. Dhaka ranks at the bottom: collections amount to approximately 0.08% of the city’s GDP. Chattogram, Gazipur, and Narayanganj barely reach 0.06% — figures that place Bangladesh not merely below middle-income peers but below the lowest-performing cities in South and Southeast Asia. For a country that aspires to achieve upper-middle-income status by 2031, this is a challenge that demands urgent resolution.

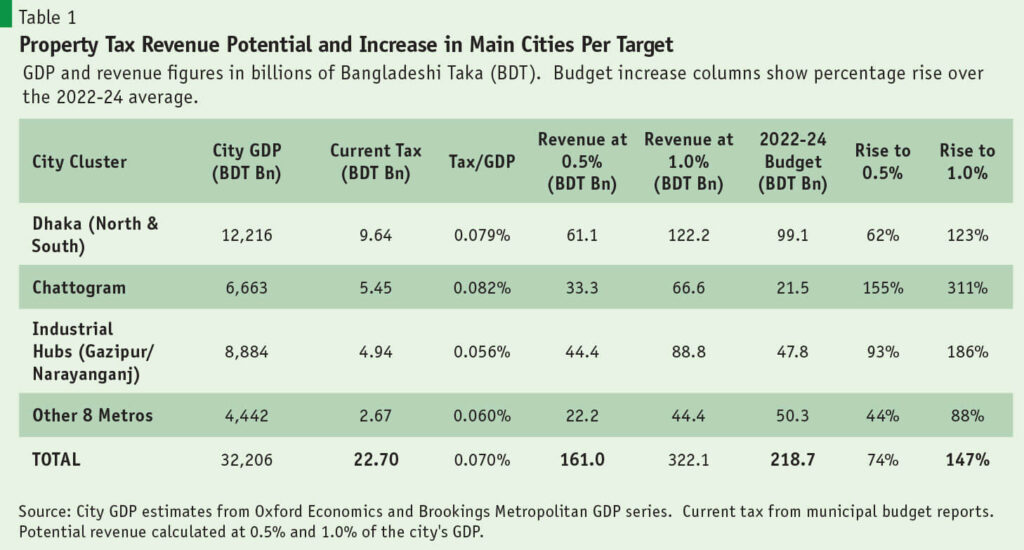

The revenue potential if Bangladesh were to reach middle-income norms is enormous. At 0.5% and 1.0% of local city GDP — a conservative benchmark for an emerging market — the 12 major metros could collectively generate an additional Tk. 161 billion and Tk. 322 billion respectively. Dhaka alone, with its extraordinary density and concentration of wealth in Gulshan, Banani, and Baridhara, could realistically reach Tk. 122 billion. City budgets would increase by an average of 74 and 147%. These targets are simultaneously modest — even at 1.0% of city GDP, the overall property tax-to-GDP ratio would reach only 0.6%, well below the NTFTR’s 1% ambition — and still demanding, requiring revenues to grow by 8 to 16 times their current level.

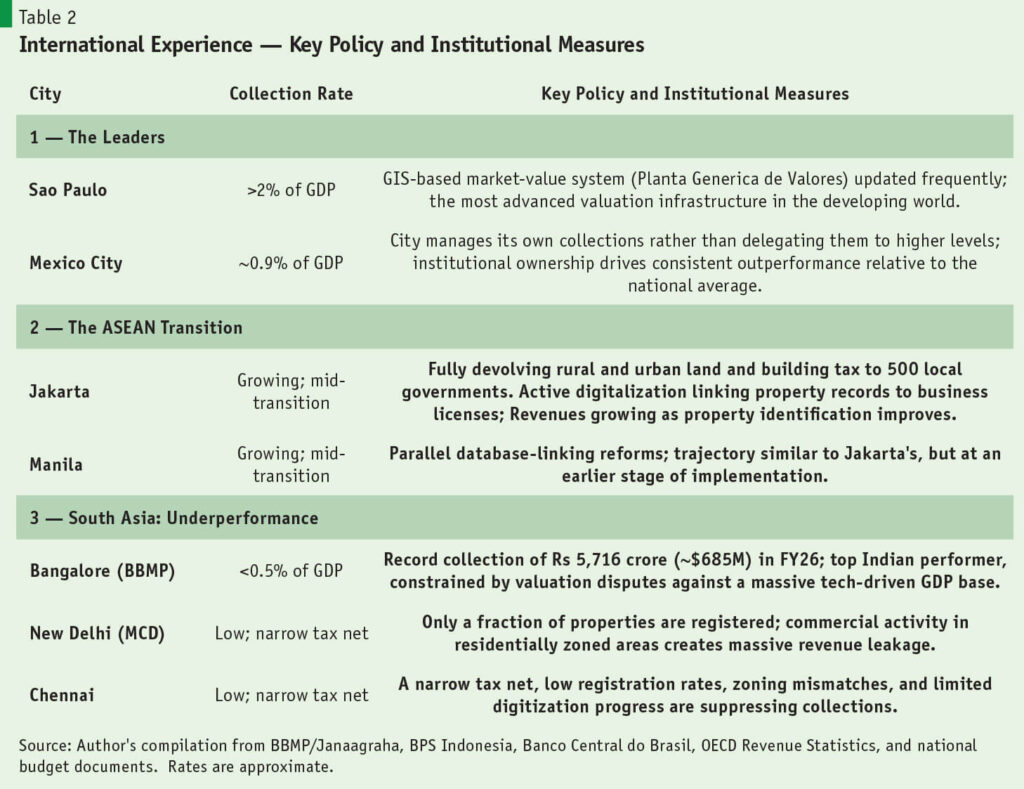

Such increases will require significant policy and institutional reform. Table 2 illustrates the policies and instruments cities across the world have adopted to collect property taxes. Three factors consistently explain high performance in international comparators such as Sao Paulo, Mexico City, and Bangalore: (i)using area-based property valuation rather than rental value; (ii) deploying GIS technology for property identification and valuation; and (iii) granting cities genuine fiscal autonomy to collect and retain property tax revenues.

In turning to the specific case of Bangladesh, this article will emphasize a graduated institutional approach—one that increases compliance more through incentivization than through enforcement, beginning where revenue potential is greatest and administrative capacity is most developed.

IV. Diagnostics: Why the Current System Is So Weak

The budgetary contribution of land and property taxes in Bangladesh has collapsed over the decades, falling from roughly 20% of total tax revenue in the early 1960s to barely 0.11 % of GDP in FY22. Thus, the NTFTR Report rightly identifies property taxation as one of Bangladesh’s most underutilized revenue instruments.

The instrument Bangladesh relies upon — the Annual Rental Value (ARV) system — is a relic of colonial administration, updated by the Municipal Corporations (Taxation) Rules of 1986, the Local Government (City Corporation) and Paurasabha Acts, 2009 and even by some rules that draw on the Municipal Act of 1881. Under it, a city assessor estimates a property’s potential monthly rent, deducts 2 months of rent as maintenance costs, multiplies the monthly rent by 10 months, and applies a 7% tax rate (plus another 10% for waste management and lighting) to that notional income.

The ARV system suffers from three structural defects.

First, it encourages evasion. Owners under-report rental income to both the National Board of Revenue and the City Corporation. Because the tax is based on declared rent — perhaps negotiated with collectors, who do not verify it — the tax base shrinks to whatever is agreed upon. In a city where actual rents have risen sharply amid strong demand, assessed values remain anchored to figures negotiated years or even decades ago. Manual assessment, conducted door-to-door with no digital verification, invites corruption and evasion.

Second, it ignores capital appreciation, probably its most costly defect. Urban land values have risen 80-fold in four decades from independence to 2011 and 28-fold in Dhaka between 2000 and 2021, making its urban land market one of the most valuable in South Asia on a per-square-kilometer basis. A tax calibrated to rental income captures only a minuscule portion of this wealth. The windfall of urbanization, which accrues overwhelmingly to landowners, escapes taxation, violating both efficiency and equity principles of urban economics.

Third, the collection machinery operated by the undertrained, unequipped staff of City Corporations and Municipalities is antiquated. There is no digital ledger, no cross-reference with utility connections or property registrations, and no mechanism to catch properties that have never been assessed. The broader, complex property transaction framework compounds the problem: there are stamp duties (1.5%), registration fees (1%), municipal and land development taxes (2%), conservancy/waste disposal taxes (of about 7%) that overlap with the holding tax rate of about 7% of the ARV in a complex tangle that encourages under-declaration of rental and sale values. Exemptions for gifts, bequests, and trusts have been compounded by Section 5 of the Land Development Tax Act of 2023, which grants authorities discretion to alter or forgive land taxes without clear guidelines, further inviting irregularities and narrowing the tax base.

V. The Reform Strategy: Five Pillars Plus Political Economy

Bangladesh’s property tax reform will need to be based on four pillars of policy and institutional change, with the first as the main driver. However, before discussing these, it is worth stressing that a fifth pillar, addressing the political economy of property tax reforms, will be key to successful implementation. That aspect is taken up in the next section.

1. Shifting from Rental Value to a Value-Based System

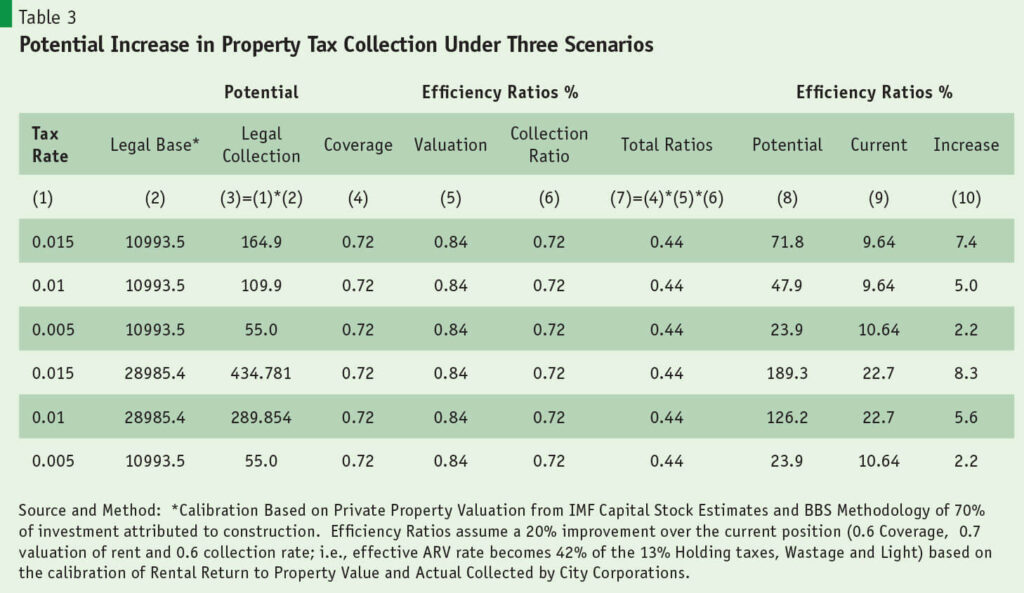

The primary structural change, the heart of the reform, will be the replacement of the ARV system with an ad valorem Value-Based System (VBS), as already proposed in the draft of the Municipal Revenue Act of 2026. Table 3 shows the potential of the VBS by using the value-based formula for tax collection:

| Total Property Tax Revenue = (Tax Rate × Legal Base) × (Valuation Ratio × Coverage Ratio × Collection Ratio) where, |

| -Coverage Ratio: The number of properties on the tax rolls divided by the number of properties legally subject to tax. |

| -Valuation Ratio: The assessed value divided by the true market value. |

| -Collection Ratio: The actual tax collected divided by the total tax billed. |

Table 3 uses a 4 percent annual rental return on property values and calibrated collection-efficiency parameters to replicate current holding taxes in the 12 metropolitan cities and Dhaka North and South. Then, conservatively assuming a 20% increase in collection efficiency under a Value-Based System following the introduction of GIS mapping and other cross-checks, Table 3 provides three estimates based on property tax rates of 0.5%, 1.0%, and 1.5%. Property tax collection increased by factors of over 2 times, 5 times and 8 times (column 10).

Although the VBS has high potential, its introduction will be technologically and institutionally demanding and take time. Given these factors, the implementation should adopt the principles below.

• A gradual approach to a VBS is both politically necessary and technically sound. As a transitional tool, transaction-based revenue collection through stamp duties and registration should continue to be used on a declining schedule to maintain stable revenue, despite its distortionary effects. However, according to the NTFTR’s recommendations, these taxes should be reduced by up to 50% to encourage greater accuracy in reporting transaction values.

• In the same spirit, reforms should start with area-based taxes (at a fixed rate per square meter) as a Value-Based System is gradually introduced. In doing so, the Government should use Fiscal rather than Legal Cadasters. Legally, Governments do not need perfect legal property titles to collect taxes. Hence, the priority should be to build a fiscal cadaster (recording building size, use, age and location) using satellite imagery, separate from the legal cadaster.

• The early stages of a gradual implementation strategy should include GIS/satellite mapping of all 12 metros, with the priority being given to the elite zones (Motijheel, Gulshan, Baridhara, Banani, Dhanmandi, Ulshi, and Nasirabad); and second, the design and passage of a more advanced Municipal Revenue Act.

• As valuation improves, taxation should move to a hybrid system. In dense, lower-value areas, area-based assessment at a flat rate per square meter can continue as the appropriate instrument. In contrast, a graduated assessment can be introduced to higher-value areas before ultimately moving to a mostly market-value-based system.

• Setting up an independent, professionally staffed Urban Valuation Authority for Cities will be key to removing political interference in the entire valuation exercise. Similarly, a parallel Dispute Resolution Mechanism can be established under fairly stringent conditions to discourage frivolous challenges.

• Tax exemptions must be strictly limited to genuine public organizations and registered charities. Asset-rich but cash-poor households — pensioners in particular — should be protected through deferral schemes allowing payment at the point of sale.

• Additional steps, such as surtaxes on vacant urban land, can deter speculation but require careful legal definition of vacancy.

• Alongside this, care should be taken to protect vulnerable populations, not only lower-income areas but also “asset-rich but cash-poor” households, such as pensioners. Governments can soften the impact of taxes on this latter group by reducing property taxes and even deferring them until the property is sold.

• The technical capacity of City Corporations’ and Municipalities’ staff will need to be enhanced through the training required. Staff training, third-party validators, and transparent dispute-resolution mechanisms are the administrative investments that will determine whether technical reforms translate into actual revenue.

2. Implement a Property Transfer Tax (PTT) on Gifts and Bequests

Alongside the introduction of a Value-Based Ad Valorem collection system, property taxes can be made more equitable and buoyant by introducing Transfer Taxes on Gifts and Bequests. The NTFTR’s Report makes the following well-considered proposals, which are standard policy instruments in advanced economies, for the Government to follow:

• Taxing intergenerational wealth by imposing a 1% tax on the fair market value of all gifts and bequests of property (both tangible and intangible) whenever ownership changes or mutates.

• Introducing inheritance taxation into the property transfer system, drastically improving wealth equity.

3. Using Technology and GIS to assess and verify will be the Backbone

• While starting with Area Based Taxes, in wealthy areas in particular, Drone and satellite data can be used to identify the footprint and height of every structure, flagging unauthorized construction, and matching buildings to property registration records. GIS surveys in comparable cities routinely discover that 20 to 40% of buildings have never been assessed. But technology should be used further to cross-reference property IDs with National Identity cards, utility meters (DESCO, WASA), and the NBR’s newly introduced scheme that integrates electricity distribution data with tax records, thereby providing robust identification of property owners. A building with eight electricity meters should be considered to have eight taxable units. The result will be a public digital ledger resistant to the negotiated settlements that define the current system.

4. Collection Through the Banking System

• The collection architecture must move entirely out of the City Corporation’s door-to-door machinery. Property tax assessment records should be made available on the City Corporation’s website, and payments should be accepted through any commercial bank or mobile financial service—bKash or Nagad—with automatic digital receipts.

• For large commercial properties, integration with annual trade license renewals or utility billing should markedly increase compliance. This shift removes discretion from the point of collection and eliminates the negotiated assessments that are the primary source of leakage.

5. Fiscal Autonomy for City Governments

Property Tax reforms are unlikely to succeed if City Corporations remain administrative arms of the Ministry of Local Government. That happens because key tax bases such as the Stamp Duty, Registration Fees, and the (Capital) Gains taxes are collected and retained by the central Government. Then, through the LGRD, it provides most of a city’s revenue through ADP grants. Further, under the Government’s current fragmented rules, Mayors have little authority over public services provided by sectoral Ministries. They are unable to carry out the critical task of coordinating interlinked public services. Thus, Mayors have little reason to invest political capital in imposing taxes that residents resist. The incentive structure must be inverted: all property and related taxes collected by the NBR should also remain with the City Corporation; mayors should set rates within a national band of 0.5-1.5%, making them directly accountable to their constituents. To reduce arbitrariness and corruption, valuation should be removed from ward-councilor politics, which currently distorts it. Instead, an independent Urban Valuation Authority should provide the assessments based on transparent market benchmarks. ADP grants should taper as property tax revenues rise. And sooner rather than later, Dhaka and Chattogram should eventually be permitted to issue municipal bonds backed by property tax streams.

To strengthen probity and accountability, it is critical that local Government Financial Management bodies, belonging to or overseen by the Central Government’s CAG office and the IMED, maintain accounting and auditing standards and provide timely public reports not only on city public finances, but also on overall City performance.

VI. Addressing the Political Economy through a new Urban Social Contract

Tax reforms can succeed only when citizens see them as an exchange for public services, not as an extraction. Bangladesh’s City Corporations have, at best, had a mixed record of delivering visible services, which is why compliance with holding tax payments is so poor. Thus, the final pillar of property tax reform will prioritize delivering visible public services linked to property tax payments, either at the same time as, or even before, the introduction of taxes.

On the incentive side, legally earmarking 50% of collected tax for visible improvements in the same ward — i.e., ward-level hypothecation — can be a potent tool for diffusing opposition to taxes. Further, regular, publicly available accounts that present information on ward-level collections against ward-level spending can motivate public interest and compliance. Residents in a high-collection ward can attest to receiving better services in return for their tax payments. To encourage compliance and promote local club goods, cities and towns can offer 5% early-payment discounts and concessions to certified green buildings that have solar panels or rainwater-harvesting systems. These incentives provide additional positive inducements.

However, the other side of the coin, tax enforcement, must be equally strong. Measures may include rules requiring a Tax Clearance Certificate for the legal transfer of property. Trade license renewals linked to tax compliance can be used for commercial buildings. To avoid litigation, preparing digital records that cannot be negotiated away will reduce transaction costs and opportunities for tax evasion.

VII. The Bottom Line: Cities as Assets

Bangladesh’s 12 metropolitan cities account for close to two-thirds of the national GDP. They are the platforms on which the next phase of Bangladesh’s economic transformation must take place. But the Governments of these cities are running on budgets that represent less than 1% of their GDPs, compared to city governments such as New Delhi and Ho Chi Minh City, which have budgets of about 6% and more than 10% of their GDPs.

That is not a sustainable path. The foregone revenue from not reforming property taxes is sufficient to double and triple city budgets. That is a foregone investment in drainage that prevents flooding, in roads that reduce congestion, in waste management that protects public health and in parks and open spaces and cultural life that make their cities attractive to university students and teachers, workers and investors that will drive the growth of their cities and the economy of Bangladesh.

Dr. Ahmad Ahsan is Director, Policy Research Institute and previously a World Bank Economist and faculty member of the Economics Department of Dhaka University. He can be reached at ahmad.ahsan@caa.columbia.edu.

Selected References

Ahsan, A. (2019). “Dhaka-Centric Growth: At What Cost?” Policy Research Institute Policy Insights, November 2019.

Alam, K. (2021). “Efficient Land Management for Industrialization and Urbanization” in Vol. 3 of Background Papers of the 8th Five-Year Plan, Agriculture, Land Management and Urbanization.

Awasthi, R., Le, T. M., & You, C. (2020). Determinants of Property Tax Revenue: Lessons from Empirical Analysis. Policy Research Working Paper 9399. World Bank Group

Bahl, R. W. (1976). Urban Property Taxation in Developing Countries. Urban and Regional Report No. 77-5. The World Bank, Development Economics Department, Urban and Regional Economics Division.

The Business Standard (2022), “Up to 2700% land price hike in two decades makes owning a home in Dhaka Elusive,” Citing the Institute of Planning and Development Study.

Martin Grote, Mario Mansour, Jean-François Wen (2024). “How Property Taxes Can Help Low-Income Countries to Develop”. International Monetary Fund Blog

Grote, Martin and Jean-François Wen (2024). How to Design and Implement Property Tax Reforms. International Monetary Fund

Global Property Guide (2026): Residential Rental Yields by City.

Kelly, R. (1992). “Implementing Property Tax Reform in Developing Countries: Lessons from Indonesia’s Property Tax”. Review of Urban and Regional Development Studies, 4, 193–208.

Kelly, R. (2004). Property Tax Reform in Indonesia: Emerging Challenges from Decentralisation. Asia Pacific Journal of Public Administration, 26, 71–90.

National Task Force on Tax Reforms (2026). Tax Policy for Development: A Reform Agenda for Restructuring the Tax System. Report prepared for the Ministry of Finance, Government of Bangladesh. Policy Research Institute

Slack, E., & Bird, R. M. (2015). How to Reform the Property Tax: Lessons from around the World. Belarusian State Pedagogical University Repository (Belarusian State Pedagogical University). http://hdl.handle.net/1807/81246

World Bank. (2022). Good Enough for Outstanding Growth: The Experience of Bangladesh in Comparative Perspective. Policy Research Working Paper 10150.

World Bank. (2025). Bangladesh Development Update – Special Focus: Urbanization as a Pathway to Boost Job Growth