Reforming the Supplementary Duty in Bangladesh: The Case of Beverage Sector

By

1. Background and Context

Bangladesh faces persistently low tax-to-GDP ratio, approximately 7 to 8 percent, which constrains domestic resource mobilization and limits fiscal space for development expenditure. This structural weakness in revenue generation creates recurring fiscal pressure and restricts the government’s capacity to finance growth-enhancing investments. Although income tax and value-added tax (VAT) are the primary sources of revenue, Supplementary Duty (SD) is a critical component of the indirect tax system, accounting for about 12 percent of total National Board of Revenue (NBR) tax revenue. SD also functions as a significant policy instrument to influence consumption patterns, particularly in sectors associated with health externalities.

The beverage industry – a sub sector of the sugar-sweetened beverages (SSBs) – is a key sector for Supplementary Duty due to sustained growth in market volume and the need to address the negative externalities linked with the consumption of sugary and salt products. Within the beverage sector, particularly carbonated soft drinks, energy drinks, and packaged juices, SD serves a dual function: revenue generation and public health regulation. The current SD structure, however, is marked by multiple rates, product-based differentiation, and discretionary adjustments. These features result in price distortions, classification ambiguities, and diminished policy effectiveness. Globally, the taxation of sugar-sweetened beverages (SSBs) has shifted toward transparent, rule-based, and health-oriented frameworks. Bangladesh’s existing system remains misaligned with these international practices. There also appears to be a significant compliance gap in revenue collections; this is gap between the theoretical revenue potential based on estimates of market size of various goods liable to SD, and the actual amounts of revenue collected.

The current Supplementary Duty (SD) tax structure incorporates multiple rate tiers. Although the SD tax aims to increase revenue and discourage excessive consumption of luxury and unhealthy goods, its current form is highly complex and regressive, hindering the development of an optimal tax system and imposing higher costs on businesses. Following Bangladesh’s anticipated graduation from Least Developed Country (LDC) status in 2026, there is a pressing need to transition from reliance on import-stage indirect taxes to a system that emphasizes direct taxation and a streamlined Value Added Tax (VAT). Consequently, rationalizing SD and VAT has become a central focus of tax reform policy aimed at enhancing domestic resource mobilization.

2. Problem Statement

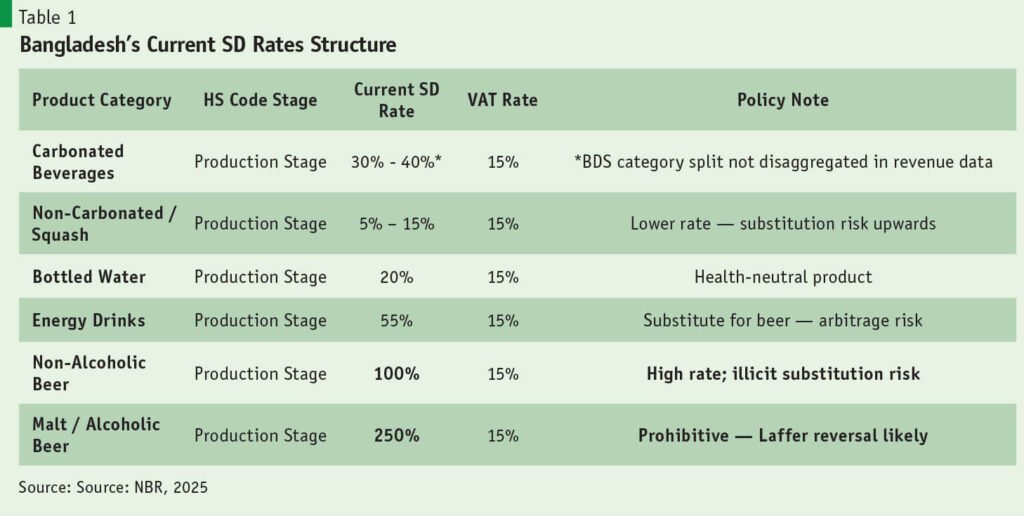

2.1 Tax structure

The current SD framework in Bangladesh’s beverage sector presents several structural inefficiencies, which undermine the SD potential and raise tax capacity. One of the major problems is the non-uniform tax structure, which means that similar products face different tax rates, distorting relative prices and consumer choice. The Finance Act 2025 reveals a beverage SD structure spanning an extraordinary range—from 5% on non-carbonated drinks to 250% on alcoholic beer (Table 1). On the surface, higher rates of harmful products might seem appropriate. In practice, these extremely high tax rates push behavior in precisely the wrong direction. Bangladesh’s National Board of Revenue (NBR) is, almost certainly, operating on the wrong side of the Laffer Curve for several categories (Figure 3).

The 195 percentage-point gap between beer (250%) and energy drinks (55%) is a particularly telling example of the structural problem. In a tropical climate, poorly refrigerated energy drinks can ferment to 1–2% ABV — functionally approximating low alcohol beer. Consumers respond to price signals; when the tax gap is this wide, substitution toward the lower-taxed category is inevitable. The government collects less from health-risky products, i.e., beer, and creates a grey zone around energy drinks that is difficult to regulate.

There is also significant disparity within the rate structures between different types of sugary beverages. The rate of tax for carbonated beverages with added sugar is more than double that of non-carbonated added sugar drinks, often with higher sugar. The tax system thus creates perverse incentives where higher sugar products can replace carbonated drinks with lower or even zero sugar options. Table 1 below illustrates the challenge.

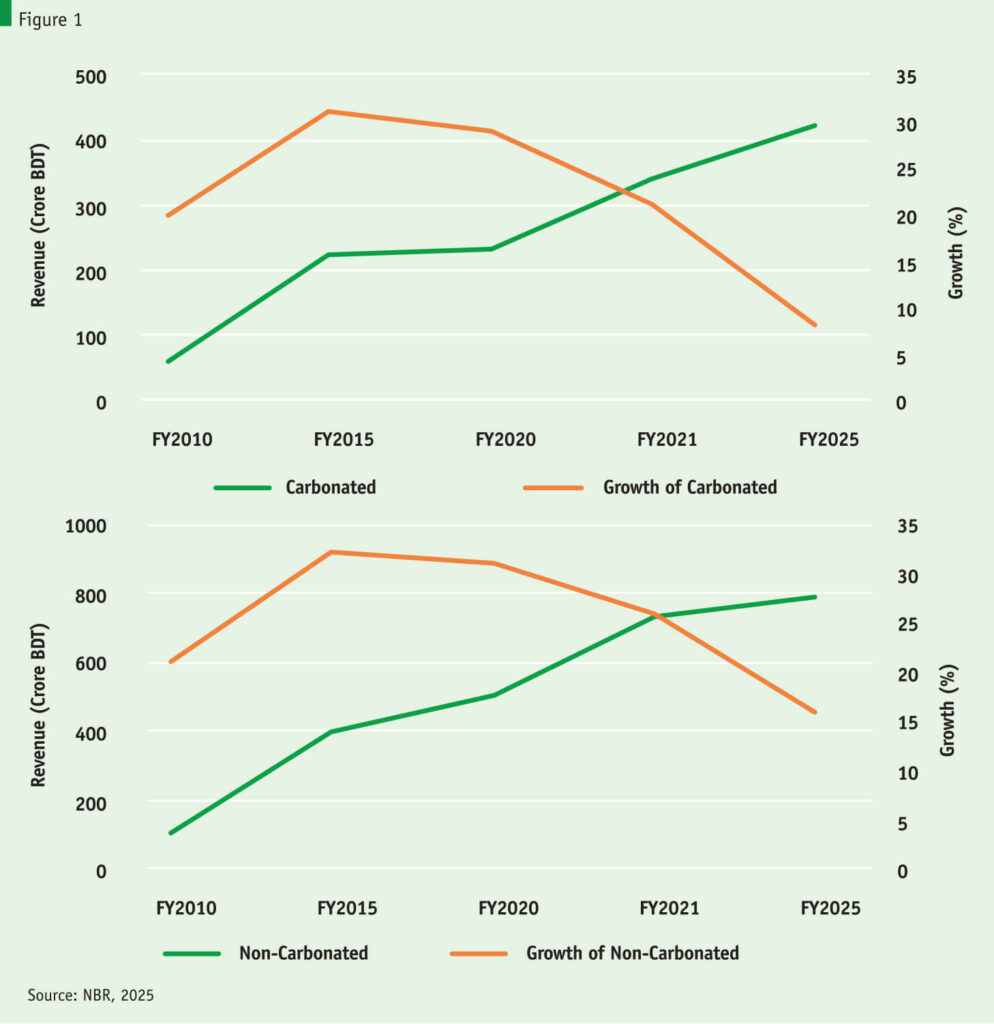

2.2 Falling revenue productivity

SD revenue from beverages has increased with the growth in the economy and increased prosperity, which appears to mask a problem of revenue productivity. Revenues from both carbonated and non-carbonated beverages have increased over the past decade. However, revenue growth for both categories slowed significantly after the SD rate hike in FY2015.

The analysis above shows that while revenue has grown the rate of growth in both categories has dropped significantly. The Laffer Curve probably explains why increases in the SD rate may raise less revenue.

2.3 Complexity of classification

A significant issue within the current SD system is the complexity of classification, which results from product-based taxation and creates incentives for misclassification and tax avoidance. The absence of taxes based on sugar content has substantially hindered efforts to internalize negative externalities. Furthermore, the existing tax structure is widely regarded as market-distorting and unpredictable in terms of policy. Such market distortion may result from unequal tax treatment, thereby affecting competitiveness among firms and across product categories. Additionally, frequent and discretionary changes in tax rates increase uncertainty for both producers and investors.

3. Global Practices and Evidence

International experience focuses on a shift toward a simpler, more effective beverage tax system. The key features of global SD tax practices in the beverage industry are listed in Table 2.

4. Reform Model for Various Revenue Scenarios

Based on the global SD structure benchmarks for the beverage industry, Bangladesh faces the following gaps: i) no sugar-content-based taxation, ii) over-reliance on product classification, and iii) weak integration with health risks. This study proposes the reform model2 focusing on the overall beverages industry and considering possible reform scenarios with additional revenue gains (SD plus VAT).

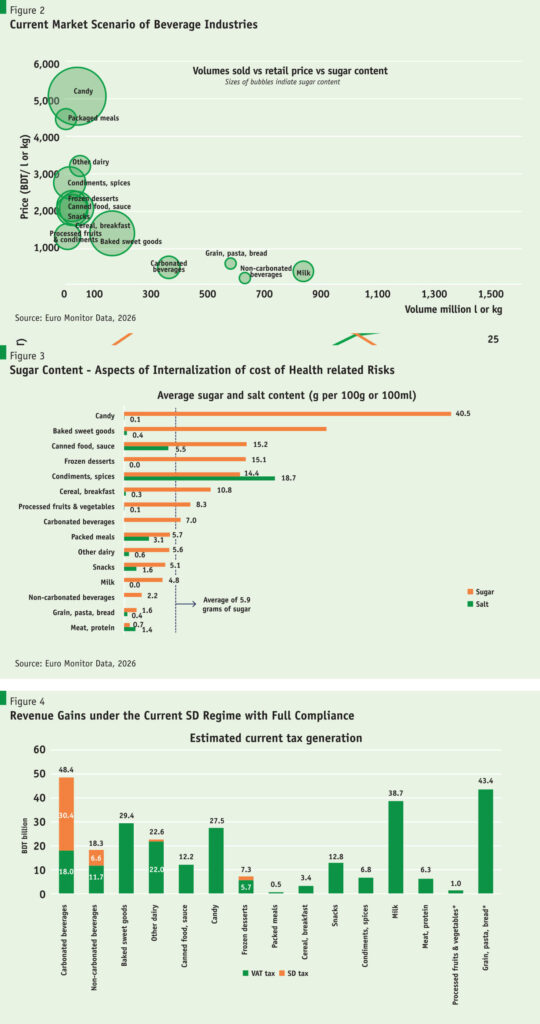

Data in Figure 1 and 2 clearly points to two important aspects of the SSB sector in Bangladesh: (i) availability of large numbers of SSB products in Bangladesh – most of which are untaxed; and (ii) sugar and salt content contained in these products – which should form the basis of SD taxation of SSB product.

Considering the above aspect of the SSB SD system, several simulations were carried out to assess the revenue, price and consumption effects of potential policy reforms: (a) full compliance SD system; (b) broadening of the SD tax bases; and (c) taxation based on the SS contents rather than on values.

Illustrative Scenario : Current SD regime with full market compliance

The objective of the illustrative scenario is to show that broad based excise (SD) taxation may generate substantially higher revenue with consumption rationalisation. According to NBR statistics, revenue collection from beverage products was BDT 61 billion in FY 2025. Against this backdrop, the illustration scenario a simulation was carried out considering broadening base (please note currently the processed fruits and vegetables, and grain, pasta, and bread are fully exempted in the current SD structure) and full compliance. The estimated revenue generation from SD and VAT is reported in Figure 1. A critical data point grounding this scenario: the government currently earns BDT 278 billion in combined SD and VAT from the packaged food and beverage sector, of which BDT 48 billion comes from carbonated beverages alone — assuming full market compliance. The modeling suggests meaningful upside from a better-designed structure that does not drive consumption underground.

The simulation exercise may be extended to show the impacts on revenue and consumption under alternative scenarios focusing on tiered rate structures, and specific taxation based on sugar content etc. Results from such simulation exercise will help NBR in discussion with the industries and develop effective taxation for SSB sector. This was discussed in general, global good practice terms during the seminar; further work could include modelling work to show possible revenue impact results including assumptions made on elasticities of demand for various types of beverages. Much of the foregoing discussion has been on the policy gap and policy interventions in relation to SD. It is also necessary to consider the compliance gap in selective taxes, given the generally poor standard of tax compliance in Bangladesh. A modern excise administration encompassing digitized flow meters and input-output controls, as well as modern, digitized tax collection can deliver significant compliance improvements in SD from beverages.

5. Recommendations

The reform framework rests on three structural corrections, followed by a phased implementation roadmap.

1. Fix the order of charge. SD and excise should be levied at a single point — the factory gate or import point — and decoupled from the VAT base. This eliminates cascading taxation and aligns Bangladesh with international best practice. This should be a medium-term goal in fiscal reforms; ultimately, a separate charging Act could be considered for selective taxes.

2. Restructure the rate architecture. Rates should reflect actual sugar content and alcohol volume rather than broad product category labels. Crucially, Laffer analysis must be used to identify revenue-maximizing rate levels — currently, this analysis is absent from the NBR’s rate-setting process. In the short term, zero sugar products should be taxed at a lower ad valorem rate than products with added sugar.

3. Move Toward Specific Taxation: The SD structure should gradually replace ad valorem SD with specific taxation. This would reduce tax evasion and price manipulation, leading to a more predictable revenue stream. If a fully specific system is considered risky, an interim solution would be to impose the tax at a fixed rate per litre of product, as is the practice in Belgium or The Philippines.

4. Rationalize the tax rate as an interim measure: The SD rate for beverages should be based on sugar content rather than applying different rates between carbonated and non-carbonated beverages while specific taxation is studied. This can be done in the present ad valorem system, applying a standard rate for all sugar sweetened beverages, which could perhaps be rationalised to 20%. Standardisation to a single rate on beverages with added sugar content can later help for differentiation of rates based on sugar content. It will also be possible to use data on market size of beverages to just run a simple model of what such a 20% rate would deliver in revenue, assuming full compliance.

5. Simplify Tax Structure: The tax authority should reduce the number of SD rates and harmonize across similar categories. This simplification of the SD rate structure would lower compliance costs and improve administrative efficiency.

6. Repair the data infrastructure. HS codes for domestic excise must be standardized. Disaggregated reporting of SD versus VAT by product sub-category should be mandated, and elasticity modeling should be commissioned before any future rate changes are enacted.

7. Introduce SD roadmap: The proposed SD rate rationalization on packaged food and beverages with added sugar will be implemented by the 2026–27 budget cycle. The development of in-house modeling capacity, structured stakeholder engagement, and a longer-term transition toward global best practices with product-specific harm-based rates can be implemented .

8. Enhance compliance processes for SD: Modernization of SD administration to include digitized flow meters as well as improved process and collection tools will increase revenue collection.

6. Conclusion

Bangladesh currently faces a significant opportunity. The packaged food and beverage sector is sufficiently large to generate substantial additional revenue. The health rationale for sugar taxation is well-established, and the available data, though imperfect, are adequate to inform policy action. The decision is not between reform and maintaining the status quo, but rather between implementing evidence-based reform and proceeding without such evidence. Aligning taxation policies with global best practices can enhance revenue efficiency, address health-related negative externalities, and improve policy transparency. Consequently, a gradual, evidence-based reform strategy will be essential to the successful implementation of the SD tax structure.