An Economic Legacy Worth Reclaiming Reflections on the FY 2026-27 Budget

By

Learning from History

Past BNP governments have a strong record of economic management that should serve as a model for the new Government. That history has become particularly relevant at a time when the economy faces multiple challenges and the newly elected BNP government, on which the people of the country have pinned their hopes, is preparing its first budget. Initial reports suggest the budget will be highly expansionary, raising questions about whether it risks destabilising the economy and undermining the new Government’s goals.

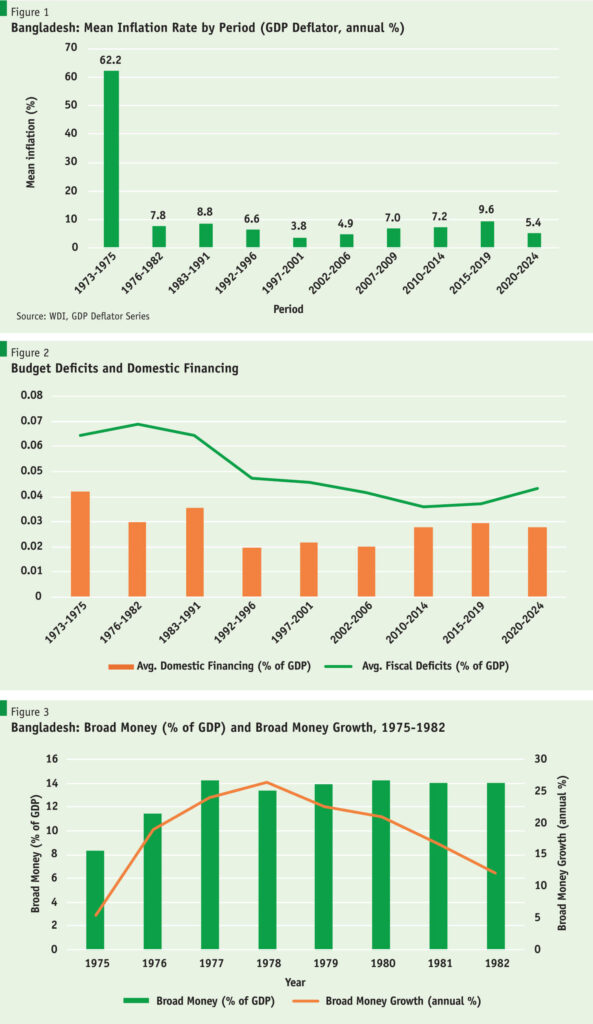

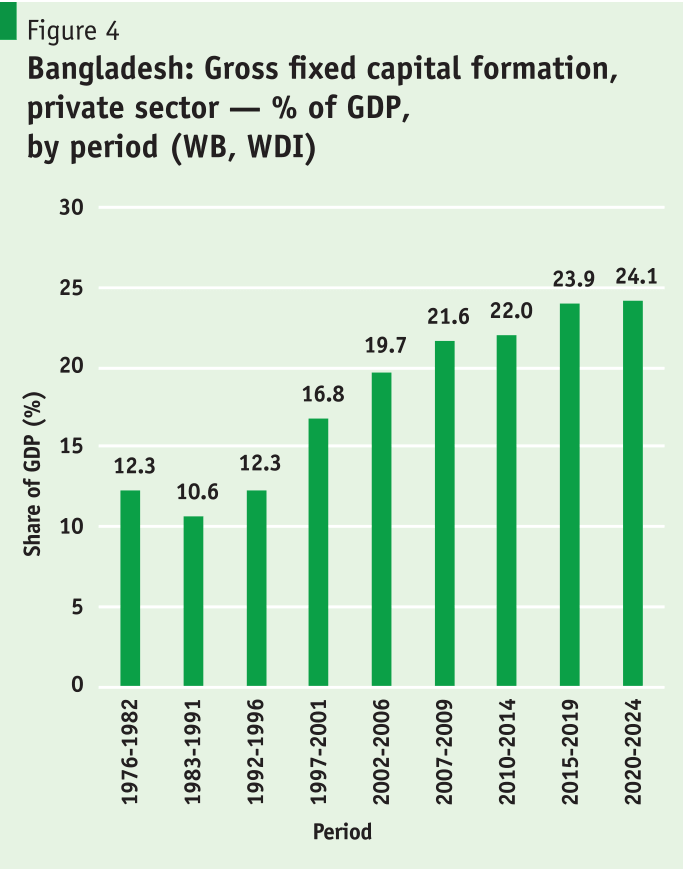

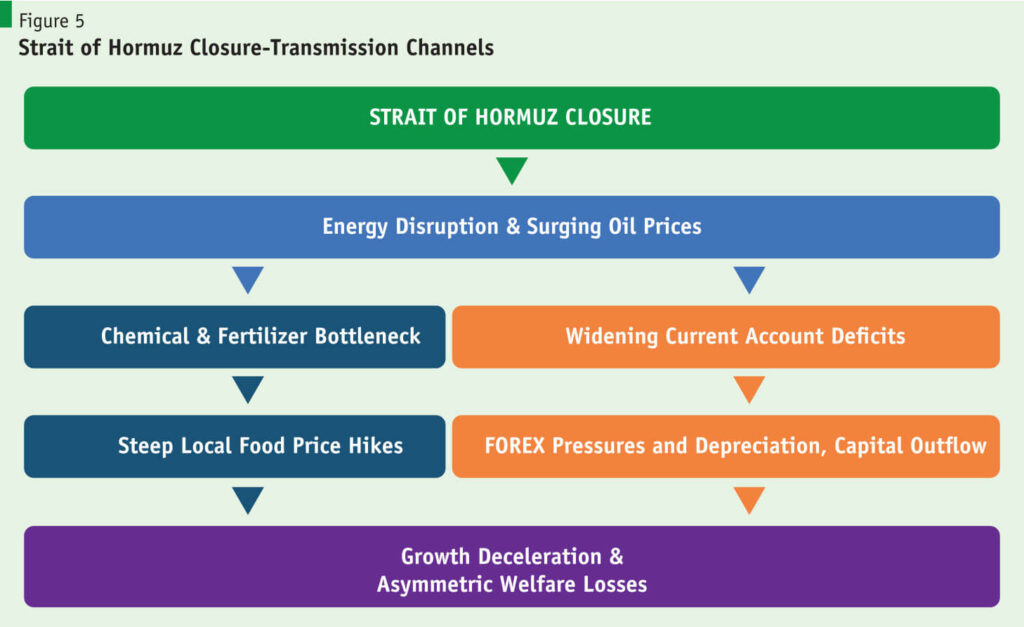

After 1975, General Zia not only steadied the ship of state but also stabilised the economy with striking speed. Inflation was squeezed from an average of 62% per annum during the three fiscal years 1973–75 to 7.8% per annum over the next seven years of the tenures of Presidents Zia and Sattar (Figure 1). That achievement was only possible through tight limits on total and primary budget deficits, a sharp reduction in domestic budget financing (Figure 2) and disciplined control of broad money supply growth (Figure 3). Despite that monetary restraint, careful balancing helped more than double the private sector’s share of credit in GDP — from 2.3% to 5.4% — in turn financing a doubling of private investment to 8% of GDP.

In doing so, the Government established a tradition of sound macroeconomic management for the next 35 years that kept the economy on an even keel, steadily expanded private-sector financing, and earned international respect. That tradition, which lasted until about 2017, became the foundation of Bangladesh’s economic and human development success that came to be admired worldwide.

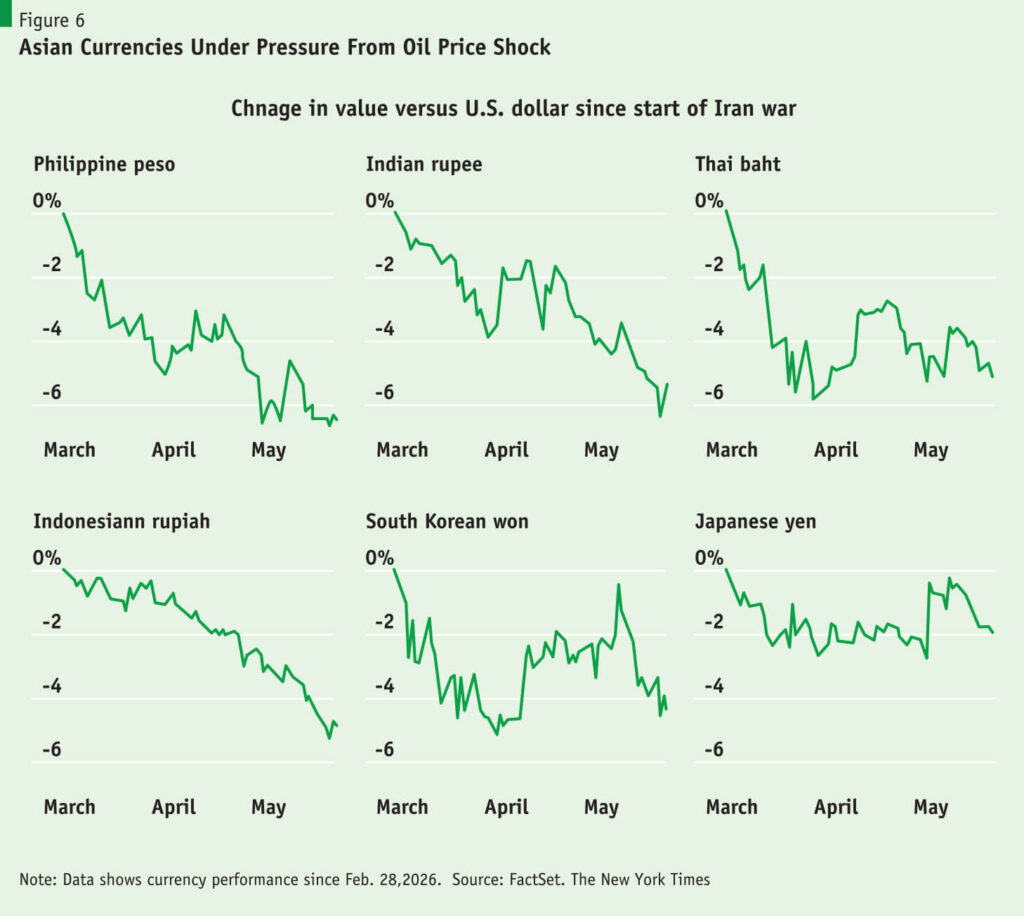

It is not an exaggeration to say that the modern Bangladesh economy was built by the next BNP government during the first term of Prime Minister Khaleda Zia. Under her leadership, and the guiding hand of a visionary Finance Minister, Saifur Rahman, the Government first firmly stabilised the economy and then set a course for a private-sector-led market economy. The introduction of VAT reduced distortions, doubled revenue, and produced the Government’s first taka surplus. That enlarged budgetary space enabled health and education expenditures to double over the 1990s. Tariff reductions and the removal of quantitative restrictions opened the economy to competition while creating opportunities for RMG exporters. Combined with deregulation, accelerated privatization, and well-targeted budgets, private investment boomed, and its share in GDP has doubled since then (Figure 4).

The third BNP government of 2001-2006 again did a commendable job of significantly reducing deficits that had widened towards the end of the Awami League Government’s tenure. Equally important, the Government implemented major banking sector reforms that empowered the Central Bank, restructured commercial banks and introduced international accounting standards, all of which halved the share of non-performing loans from 31% to 14% in 2006. Current account convertibility and managed flexible exchange rates improved export competitiveness. Led by exports, growth accelerated to 5.4% per annum, accompanied by a significant reduction in poverty rates.

The reason these earlier BNP governments could do so was straightforward: their leaders took the economy seriously and surrounded themselves with the most competent economists. General Zia drew on heavyweights such as Professor M. N. Huda, Messrs. Saifur Rahman and Amir Khasru M. Chowdhury (the latter as an effective Commerce Minister), as well as highly experienced civil servants. Prime Minister Khaleda made the transformational decision to appoint Mr. Saifur Rahman as Finance Minister as a technocratic appointee even after he lost his race in the 1991 elections. One important result of having such leading lights in past BNP Cabinets was that governments were keenly conscious of the economy and economics: bold in their policies and reforms, but clear about macroeconomic fundamentals.

Laudable Goals, Fragile Economy

One of those fundamentals is preparing strong budgets suited to the times, and not relying on excessive Bank financing or, worse, printing through Central Bank borrowing. The forthcoming FY 2026-27 budget will be a test for this Government to demonstrate its understanding and competence in managing the economy.

The Government’s stated intentions are laudable: to foster economic recovery and reignite growth; to implement State-governance reforms; to create a non-discriminatory, equitable society, including, innovatively, a much-needed spatial policy to make Chattogram a regional logistics hub.

The economy is indeed in a low-level trap, with growth falling for three consecutive years to decades-low rates. The employment situation is dismal, with shrinking manufacturing jobs and declining employment, including a record 2 million jobs lost in manufacturing and services, while real wage growth has been negative for a few years. Private investment, which had been shy for some years, actually contracted in FY 2025 for the first time in 35 years.

In normal times, such an economy would indeed call for counter-cyclical expansionary fiscal policies to raise demand, jobs and incomes. However, the current slowdown is mainly on the supply side, driven by the COVID period, the war in Ukraine, political instability, and now the global energy crisis created by the war in Iran. The economy is also fragile, with risks converging from several directions. These include inflation that remains sticky at 9%, driven by continued growth in remittance-driven reserve money and supply-side structural factors, including energy prices and market capture. What must not happen is to allow inflationary expectations to become entrenched.

The reality is that, mainly due to energy supply disruptions and oil and gas prices rising by 50%, the IMF estimates real GDP growth persisting in a low-level trap well below the high growth rate of the pre-COVID era: 4.2% in 2024, 3.5% in 2025, rising to 4.7% in 2026 and falling again to 4.3% in 2027. The lower growth path results from energy price shocks spilling over into higher fertilizer, chemical and domestic food prices, as shown in Figure 5. In parallel, there will also be pressures on current account balances, exchange rates and capital outflows.

These shocks are being felt around the world to varying degrees. Even the United States, with its plentiful domestic supply and exports, has not been immune, with retail petrol prices rising by nearly 40% since the start of the Iran. However, it is the Asian economies that are singularly dependent on Gulf energy imports that have been most severely impacted. In the first month after the start of the war, an estimated $52 billion has flowed out of stock markets in import-dependent Asian economies, leading to significant currency depreciation, as seen in Figure 6. Most hard hit have been the economies with large fiscal deficits such as India, the Philippines, Thailand and Indonesia. Notably, India started the year with historically high reserves of $724 billion, enough to cover 11 months of imports.

Comparatively, Bangladesh’s buffer is thin, with foreign exchange reserves now providing about four months of import cover. A potential decline in remittance flows, significantly higher energy and fertilizer import costs, and, importantly, markedly increased government spending that leads to adverse expectations and loss of confidence can quickly trigger exchange rate instability and a decline in reserves.

Underneath it all lies the specter of Bangladesh’s fragile banking sector, with record non-performing loans of 30% of total lending and dangerously low capital adequacy ratios, requiring injections of close to Tk. 3 trillion, or less if a restructuring programme is executed decisively. Not surprisingly, the rating agency Fitch has placed Bangladesh on a negative outlook due to these risks.

In this context, unless the budget prioritises addressing these risks, it may destabilise the economy rather than consolidate it. However, as we will note at the end, challenges also present opportunities.

A Budget That Could Destabilise the Economy

Unfortunately, the budget parameters being reported in the Press are patently unrealistic and carry genuine risks of destabilization through large deficits and unsustainable deficit financing. By proposing a record budget relative to GDP, the gap between expected revenue and spending ambitions will require historic borrowing. Three numbers tell the story.

The overall fiscal deficit is projected to widen to Tk 2.70 trillion — pushing the deficit-to-GDP ratio well above the 3.5% that Bangladeshi governments had maintained until about 10 years ago. Second, more than the percentage of GDP, it is the size of the deficits that counts for a large economy such as Bangladesh. Third, to finance the deficit, the Government proposes to borrow Tk 1.50 trillion from domestic markets, of which Tk 1.20 trillion would be borrowed directly from the commercial banking system through Treasury bills and bonds, with the remainder financed externally.

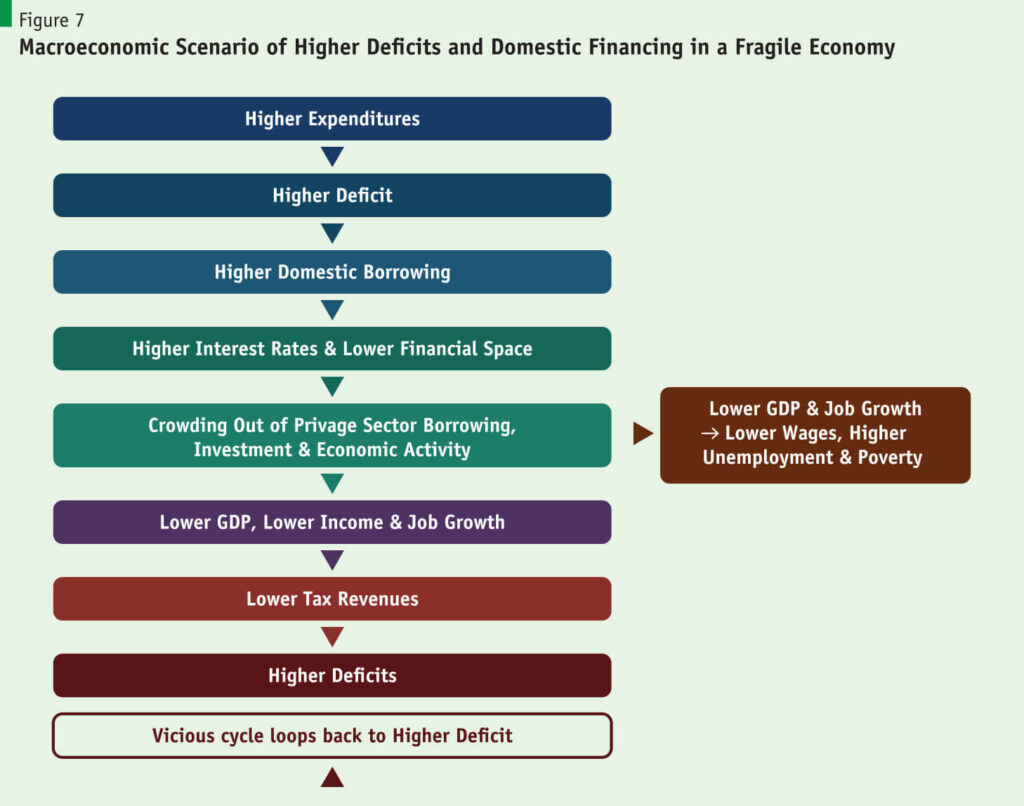

Such a massive domestic borrowing requirement will exert significant upward pressure on interest rates, crowding out private-sector activity and investment at precisely the moment the economy most needs them. Ultimately, the economy will likely see lower economic and job growth than would have occurred with more fiscal restraint. Further, one can envisage lower revenues, which would increase deficits in a vicious loop, as shown in Figure 7.

There’s an even darker scenario in which the Government also borrows directly from the Central Bank, in effect, through money printing and an increase in high-powered money. That can create a vicious higher inflation, depreciation and interest rate loop that can push the economy into a full-blown crisis: inflation generates pressure for exchange rate depreciation, depreciation feeds back into further inflation, the current account deficit widens, foreign exchange reserves come under pressure from both capital flight and government intervention to defend the taka. In short, as Figure 8 shows, this is the perfect macroeconomic storm scenario that Bangladesh experienced in 2022 and from which we have not recovered.

![]()

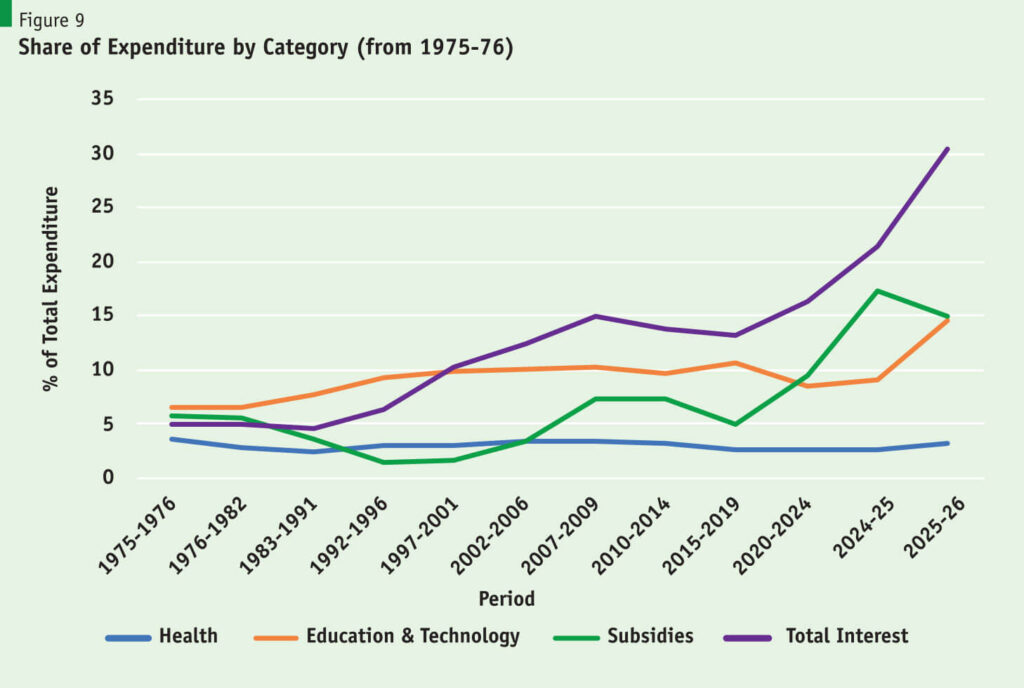

However, it is not only short-run instability that is at stake; medium-run budget scenarios are also unsustainable because they squeeze fiscal space. Because of irresponsibly high fiscal deficits and borrowing by the Awami League government, interest payments doubled between 2017 and 2022 and have now quadrupled since 2012. Interest payments now exceed the combined expenditure on health and education. Put another way, one-third of all tax collections now go to finance interest payments. Further, if we add the subsidy and subvention bills to debt servicing, then the fiscal space for running the Government and other development expenditures has been squeezed from 6.5% of GDP to 4.8% over this period.

The proposed budget numbers thus seem to continue the tradition of the Awami League’s Finance Minister, Mustafa Kamal, of running large primary deficits and increasing the debt-servicing burden.

However, that is only half the story. The other half is that if the Government continues in its reported budget expenditure plans, the deficit will be much larger. The revenue projections rest on growth assumptions that are, at best, doubtful. The budget has anchored its FY27 real GDP growth target at 6.0 to 6.5, as a successful outcome of the Government’s strategic push to return to a high-growth path. But the three major multilateral institutions project growth more modestly: The World Bank projects 4.6, up from its 3.9 estimate for FY26, assuming post-election stability normalizes supply chains. The ADB envisages 4.7% growth for FY27, citing a recovery in household purchasing power as energy shocks in the Middle East recede. The IMF is the most cautious: it projects growth to decelerate slightly to 4.3 in FY27, citing fiscal tightening, structural revenue deficits, and the banking sector’s extreme provisioning gap.

That said, the Government’s nominal GDP growth target of 15% is achievable if one assumes a lower GDP growth rate of about 5% and a higher inflation rate of close to 10%. It is reasonable to set that as the baseline, and it will be used as such in the discussion below.

So, what is to be done?

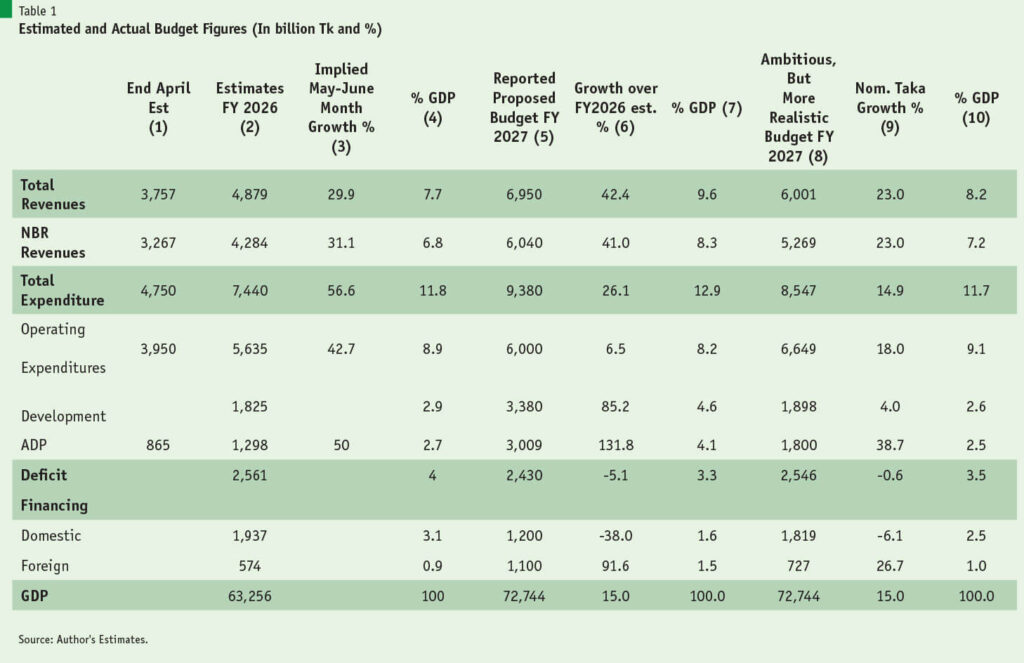

Prepare a Realistic Budget: If we are to avoid the dismal, destabilising scenarios presented above, the budget must be placed on a more realistic footing. Table 1 below presents my FY 2025-26 estimates, the reported proposed budget and, in my opinion, a more realistic but still ambitious scenario. Columns 2-4 present the estimates for FY 2026, their implied growth rates and their shares of GDP. Columns 5-7 present the parameters of the proposed FY 2027 budget as reported. Finally, Columns 8-10 present the parameters of a still ambitious but more realistic proposal for FY 2027.

The first step will be to put revenue targets on a sounder footing. The current proposal for over 42% revenue growth next year (col 6, below), while nominal GDP growth is 15%, defies economic logic and is reminiscent of the budgets of the second half of the 2010s, which many, including myself, questioned.

effort with a buoyancy of 1.5, i.e., revenue growth of about 23% (column 9), which would be in line with the IMF’s proposed target of increasing revenues by 0.5% of GDP over the next few years. Notably, and as discussed later, such an increase will require multifold reforms in policies and implementation.

The next step is to return to sensible budget deficits based on realistic and desirable financing parameters. As stressed from the beginning, the goal is to reduce domestic financing needs. Again, the past governments’ record is instructive. In general, the governments from 1991 to 2008 maintained a conservative stance, with lower deficits around 3.5% of GDP and domestic financing around 2% of GDP. The dam on both fiscal deficits and domestic financing broke only after 2009 and especially after 2014, when deficits crossed 4% and domestic financing reached nearly 3% of GDP. Notably, while the Government’s proposal slightly reduces the deficit, if it persists with its expenditure plans, the deficit could reach nearly 5% of GDP, requiring massive domestic financing.

In the current difficult situation, when risks are plentiful and emergencies can arise, the fiscal powder must be kept dry. Given the banking system’s fragility, funds must be kept available for bank capital injections, along with substantial payments and subsidies for energy, fertilizer, and possibly food imports and food relief. It is therefore prudent to keep deficits to no more than 3.5% and domestic financing to about 2% of GDP. Otherwise, the economy will end up in the same situation as in the current fiscal year, when private-sector activity was stymied by credit growth of only 4%.

Given the recent record of external financing of an average of Tk. 613 billion over the last three fiscal years, the current fiscal and economic stress that even advanced countries are undergoing, and the difficulties in negotiating an IMF programme, it may be sensible to keep the foreign financing requirement at around 1% of GDP, which takes us to Tk. 727 billion, still a marked increase from the average of the last three years.

Using ambitious revenue and responsible deficit projections, the expenditure cap is set at Tk 8.2 trillion. Accommodating a partial phase-in of the increase in civil service salaries reported at around Tk 300 to 400 billion, or 4 percent of all expenditures, and assuming some savings in the current budget, operating expenditure growth is set at 18% (9% of total expenditures). That provides fiscal space for the ADP, which stands at about Tk. 1.8 trillion, or 2.5% of GDP, much less than the proposed Tk. 3 trillion budget.

Understandably, this will be deemed unacceptable at first glance. But it should be noted that even this proposed ADP size would be at least 33% higher than what is likely to be implemented this year. Further, even these constrained targets are based on ambitious revenue and foreign financing parameters that will require strong revenue measures and focused, competent budget execution.

Set Ambitious but Achievable Revenue Targets: This article does not have space to discuss revenue and expenditure measures in detail. However, suffice it to say that the National Tax Force on Tax Reforms has provided thoughtful, comprehensive policy proposals that address both raising revenues and making the tax system more efficient and equitable. Foremost among these are sharply reducing tax expenditures, expanding the tax base, simplifying and reforming dysfunctional VAT structures and focusing attention on compliance through simplified tax submissions, incentives and stricter, well-targeted enforcement that can generate nearly Tk. 400 billion net, even after reducing trade taxes. Reforming property taxes can add another half point, eventually reaching a full percentage point of GDP, providing another Tk. 350 billion while also being equitable, promoting local governments and improving public services (as discussed in another article in this issue). However, these gains can only come with tough policy decisions,

Prioritise Expenditures and Make Expenditures Effective: Given the tight fiscal environment, the biggest impact will come from targeted, prioritised expenditures focused on key sectors and the effective use of those funds. The Government’s goals of expanding social safety nets and reviving the economy are indeed laudable. However, its expenditure plans need careful thought.

Let us first identify three critical areas to prioritise in public expenditure programmes. We will start with employment, given its immediate importance for social welfare, but note that the other two, provisions to provide adequate energy and power supply over the medium term and strengthening the fragile banking sector, will be make-or-break for the economy.

There is a need to focus on providing productive jobs for the two to three million who have left their jobs in the last two years, and for the two million new entrants to the labour force each year. That is a situation that has resulted in an increase in poverty by nearly 2 million persons. That is a high social and political priority as it may lead to social unrest. The Government aims to use a Tk. 600 billion subsidized, directed bank lending programme to create employment by reopening closed factories, supporting SMEs, agriculture and export diversification. It is a complex programme for opening closed factories, fraught with risks for the relatively financially healthy Banks that will lend to them. That will require time.

In the same vein, launching long-gestation, capital-intensive, low-employment-generating infrastructure investments, such as the proposed Padma barrage, in this crisis year will be counterproductive. It will absorb resources without delivering employment or boosting demand.

A better approach to creating jobs is to provide jobs to maintain and rehabilitate light infrastructure that has long been neglected and underfunded by a factor of 2 or 3, per my earlier estimates. These light infrastructure construction works, which fit in well with the BNP’s canal-digging programme, can include non-highway district and rural roads, river and canal cleaning, waste disposal and, most innovatively, solar panel installation. These works can be productively combined with effective training programmes to build human capital and deliver long-term earnings and productivity gains. There are highly experienced and globally respected institutions in Bangladesh, such as the PKSF, that have a wealth of expertise in this regard. There are also other successful international programmes from which lessons can be learned.

Providing jobs and earning opportunities to the people in distress is more than a matter of earnings. It is a matter of dignity. No cash transfer programme can replace that. It is worth noting that the Government’s family card and farmer card assistance programmes should be used to integrate Bangladesh’s large, mostly uncoordinated social safety net programmes and make them more effective.

The equally important task is the energy crisis that is crippling the power sector and industry. Incentives to stimulate production and investments will go nowhere if producers do not have adequate energy and power supply. Thus, the budget needs to provide resources for LNG, LPC, and petroleum imports and distribution facilities by adding FSRUs, land-based terminals and supply pipelines. Rapidly boosting solar energy supply and investments in Battery Energy Storage System (BESS) capacity to meet nighttime peaking demand are other areas that need financing. Plans to entirely pass these expenditures and investments off-budget to the PDB and BPC, and to leverage their economies of scale and negotiating power to secure lower energy prices that will finance operating and investment needs, are not realistic.

Other important steps are also known and discussed in my previous article in the February issue of Policy Insights, “Bangladesh Development Under Democracy – The Opportunity Has Returned.” What is needed is a living five-year energy and power supply strategy prepared by experts residing in Bangladesh, who will, no doubt, welcome inputs from development partners abroad.

The third critical priority is budgetary provisions to shore up the Banking sector. If not vigorously addressed, the frighteningly low risk-weighted capital adequacy ratios of the banking system and the high share of non-performing assets can plunge Bangladesh into a full-blown macro-financial crisis. Although these toxic assets are concentrated in a relatively small number of banks, the Government’s mixed signals on banking sector governance can undermine confidence and invite contagion that could put the entire system at risk. The Government has to squarely address the doubts about governance created by mixed signals that the defaulters and the looters of the Banks will be rewarded not only by returning ownership of them but also by being granted rights over the large amount of injected capital. The budget can send the right signal by presenting a public-private partnership plan to inject capital into the Banks following necessary restructuring.

Make Expenditures Effective through Financial Management: There is an understandable eagerness about speed, about the need to showcase its grand plans. However, what Bangladesh cannot afford is wasteful mega-programmes and mega-projects. The saying goes, haste makes waste. Let there not be haste makes grand-scale waste. It will also require prioritising budget and economic management reforms by strengthening accounting and auditing, and implementing quarterly fiscal reporting. In general, modern complex economies such as Bangladesh’s require high-quality, timely economic data, something that the highly dynamic East Asian economies pay close attention to. The budget should provide those resources as part of its reform plans.

Finally, as part of the goal of state reforms, the next budget should reduce the ADP fetishism of the past decade and instead prioritise filling critical vacancies in public education and health, and funding operations and maintenance, where there has been systematic underspending for years. Spending less but spending better is not a counsel of timidity — it is the only credible path to restoring investor confidence and putting the economy back on a sustainable growth trajectory.

An Economic Legacy Worth Reclaiming

The BNP’s economic legacy is real, documented, and worth reclaiming. The governments of Presidents Zia and Sattar and Prime Minister Khaleda demonstrated that sustained growth can only be achieved through disciplined macroeconomic management. The BNP governments of the past built that foundation on which Bangladesh’s remarkable development rested. The current Government should take the opportunity to build on that tradition, not depart from it by following the ill-thought-out expansionary budgets of the 2010s that helped create economic instability in Bangladesh.