Why Bangladesh Did Not Have A Revolution In Renewable Power?

By

Bangladesh’s energy security still remains in peril despite massive investments in power generation and distribution systems during the 17-year rule of the Awami League Government. Massive investments in power generation using import-based LNG, coal and nuclear power plants have made the power sector import dependent and more vulnerable to global geo-political and economic shocks. The Power Purchase Agreements (PPAs) were for the most part in favor of the Independent Power Producers (IPPs) of domestic and foreign origins, both in terms of guaranteed minimum volume of power purchase at inflated agreed prices and uneven risk sharing between the parties. The PPAs were structured in such a manner that all risks—energy price shocks, exchange rate movements, sovereign country risk, demand shifts over the long term—were shifted on to the government while ensuring very attractive rates of return on investment by the foreign and domestic power producers. The results are predictable: excessive investment in power generation, far in excess of domestic demand; ballooning of the public sector subsidy bill over the years; high domestic power tariffs, compared to most comparator countries, to partly offset the losses in power generation; and lack of investment in power transmission and distribution network.

This policy also gave rise to a powerful fossil fuel lobby undermining realization of Bangladesh’s renewable energy potential and continued excessive dependence on import dependent liquid fuel for the transport sector. Bangladesh is nowhere near its stated national objective of [20%] of power generation by 2025 and to [30%] of power generation by 2030. Renewable power generation capacity in Bangladesh currently accounts for only 2.1% of the total installed capacity in 2026. The switch to Electric Vehicles (EVs) was never encouraged through proper incentives for buyers of EVs, and in the absence of proper recharging infrastructure along major highways. As such, the switch from liquid fuel based combustible engines to EVs has not even taken off in any real sense. The continued high dependency on fossil fuels has also given rise to Bangladesh’s chronic energy insecurity, which has only exacerbated by the ongoing US-Israeli launched war on Iran.

Against this background, in this policy note we would like to:

(i) Identify what can be done quickly to reduce pressures on the budget through reduced subsidy and on the balance of payments through reduced import payments associated with power sector operations and investment.

(ii) Restart Bangladesh’s renewable energy program, driven primarily through an ambitious solar power generation strategy which will be highly cost effective for new IPPs interested in renewable energy, and also allow for wider participation of all types of industries, public sector entities ( like Bangladesh Railways, Tea Board, and agencies in charge of public lands and water bodies) and the private households in the form of roof-top and other forms of solar panels driven expansion of the current “Buy-Back” policy and other appropriate policies.

(iii) Appropriate rebalancing of risks between the power producer—be it conventional or renewable– and the monopsonic public sector utility companies (buyers).

(iv) Launching an EV revolution in Bangladesh through a combination of incentives for import and domestic manufacturing of EVs, and public policy driven expansion of EV charging station across the country in a cost-effective manner.

1. Renegotiation of Power Tariffs and Rebalancing of Risks in the Existing and New Contracts

The former Awami League (AL) government had signed a host of medium- and long-term PPAs with domestic and foreign power produces. Initial ones were quick rentals followed by large gas and coal-based power plants. Contracts for most of the quick rentals had expired and some are still running on extended contracts without capacity payments. There are numerous other dual fuel (gas and furnace oil) power plants operating under long-term contracts each of which can be renegotiated to reduce their tariff rates and capacity payments to more reasonable levels. Summit Power, the largest IPP in Bangladesh, had offered to reduce the tariff rates to more reasonable levels during the Interim Government period which can now be taken up to arrive at a more rational and reasonable tariff and capacity payments through negotiations. The PPA with Adani Power of India needs to be reviewed comprehensively and negotiations can be restarted, if possible, with support from the Government of India while trying to avoid involvement of international arbitration.

The Ministry of Power and its associated agencies have been incurring huge subsidies under normal circumstances due to one-sided PPAs which are not sustainable from budgetary point of view. Even a partial pass-through of the implied long-term marginal cost of power generation often leads to high levels of customer tariffs–despite huge and unsustainable subsidy burdens being incurred by the government–giving rise to affordability issue at the household level and making industries and businesses uncompetitive.

The Interim Government had taken some initiative to revise the PPA terms more in favor of Bangladesh with mixed results. This initiative needs to be pursued more seriously by the successor new government with large power companies like those with the Adani Group of India, Payra Power Plant’s Chinese investors, SS Power’s Majority Chinese investors etc. Summit Power, had offered to the Interim Government for revising/renegotiating the power tariffs in favor of the Government. Summit Power also offered to make more than a billion dollars in new investments in the solar power segment. The Government can establish a panel of experts to reopen negotiations for better terms. Such renegotiations, while expected to be difficult, have been done in several other countries and can be done in pragmatic ways ensuring reasonable (but not excessive) returns for the investors and avoiding political rhetoric.

In addition to tariff renegotiations, rebalancing of future risks sharing between the government and the IPPs should also be pursued in a systematic manner. Exchange risk may be borne by the government since it is determined by quality of government’s macroeconomic management and external/exogenous economic, security and political shocks beyond the control of private investors. However, there may not be any need for sharing the exchange risks for solar power projects since since unlike fuel-based power plants, solar/wind power plants do not need to import fuels to their operations. All other risks, like movements in petroleum or LNG prices (unrelated to exchange rate movements), global transportation problems, etc. should be borne by power producers/investors as normal business risks.

2. An Expeditious Launching of Bangladesh’s Renewable Energy Program

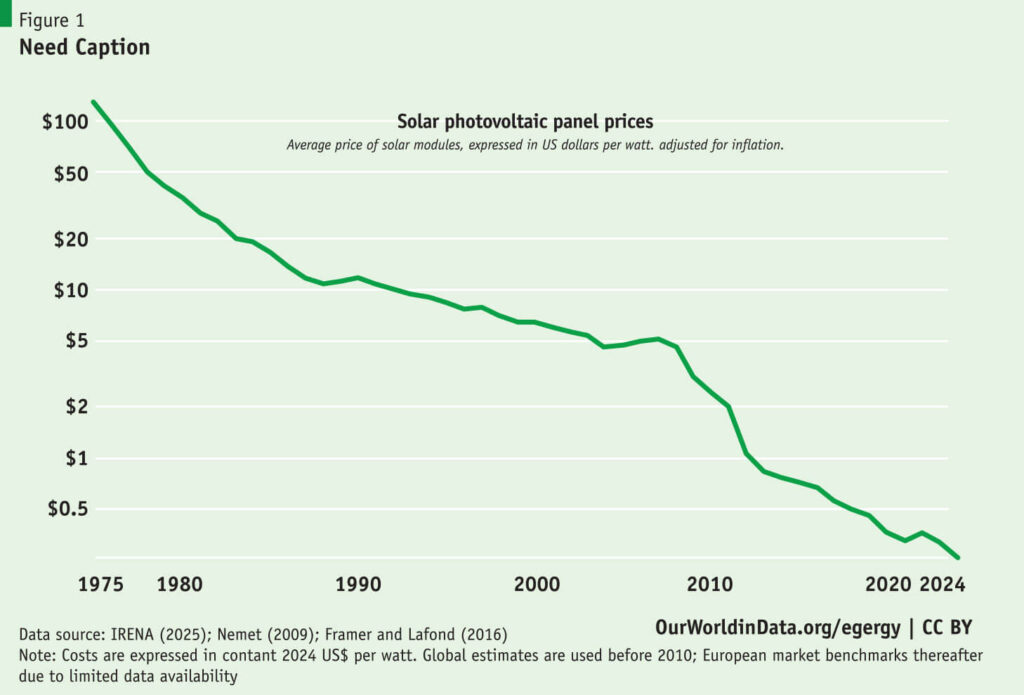

Cost of solar panels has declined by more than 90% over the last several decades (Figure 1). Solar panel prices have fallen nearly 99.8% since 1975 and over 94% since 2008. What used to be the most expensive source of power—often considered wishful dreams of green energy lovers never to be realized given the high cost of solar power generation—started to become the cheapest form of power. In many ways the renewable energy—primarily in the form of solar and wind—started to become more and more people centric but as complementary to the large-scale power generation by the corporate sector IPPs. An interesting model was developed in some European countries—including Germany, which I had the opportunity the closely observe at the invitation of a German nongovernment thinktank. Large wind turbines were set up in the back or front yards of German farmers with financial and technical support from the government and with fixed-price buyback provision to encourage the farmers to become wind power producers. A farmer with two large wind turbines in his land could produce 4 MW of power even as early as 2012. In the meantime, generation capacity of turbines have also increased to 4-6 MW per turbine, with each German wind farms generally having 5 to as many as 150 turbines of 4-6 MW each. Total onshore wind power generation was 63,461 MW in Germany in 2024, with new additions of 3251 MW power in the same year through erection of 545 new wind turbines in the same year.

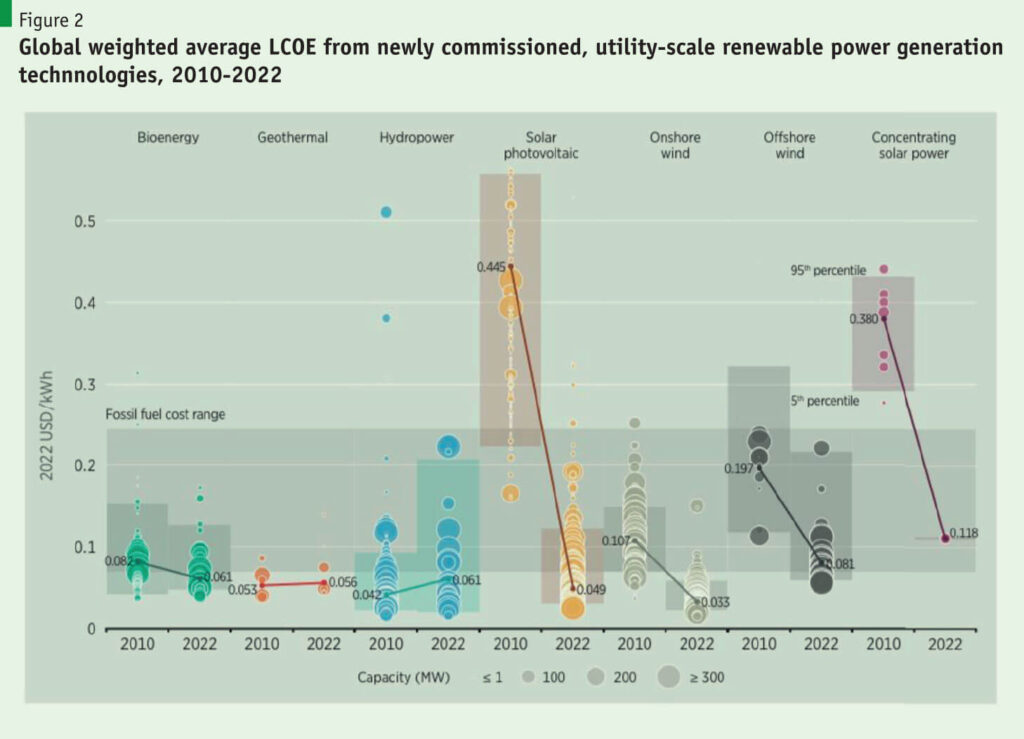

I am highlighting the German example just to illustrate how government policy support—in the form of “buy-back” arrangement under pre-agreed terms–can usher a decentralized, small-scale, household/farm-based revolution in renewable power generation. Along with drop in solar power cost, wind power generation costs have also come down with improvements in technology and generation capacity of each new wind turbine. In general, we keep underestimating learning curves for clean energy. Costs for both wind and solar—as shown in Chart 2 below–have plummeted from 2010 to 2022 and beyond: Solar PV: -89%; Onshore wind: -69%; offshore wind: -59%.

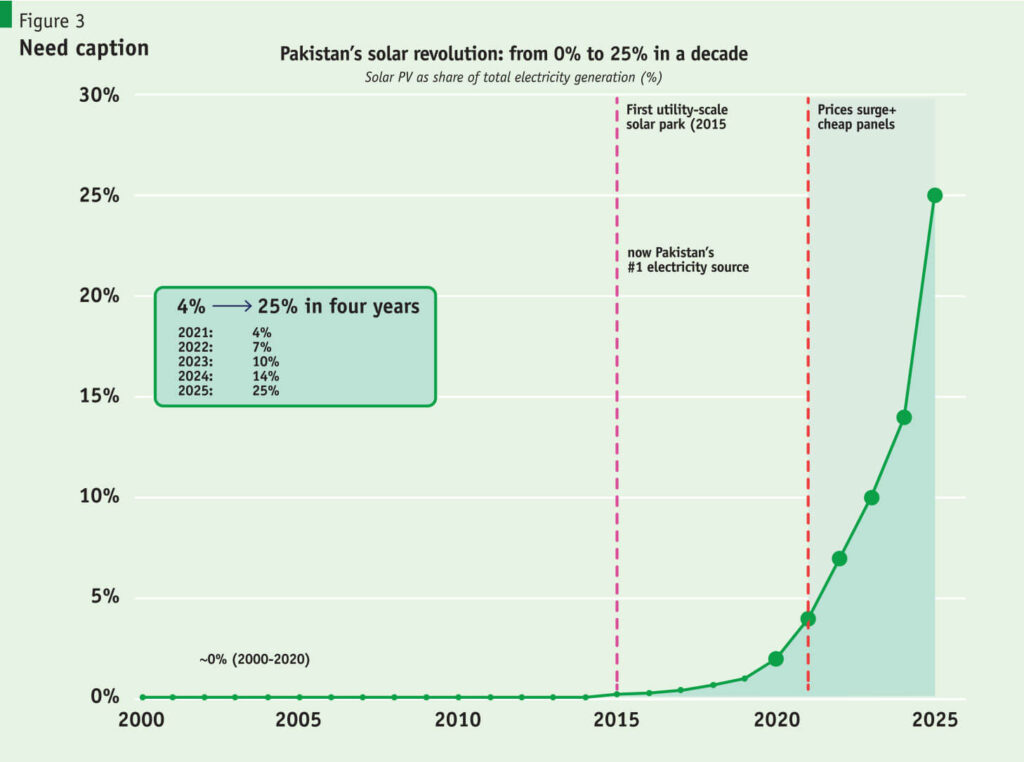

Pakistan is another excellent example of such a revolution at a more micro level in solar power in recent years (Figure 3). Pakistan’s massive grassroots solar revolution has increased the share of solar powered electricity from near-zero to over 20% in just a few years. Millions of households and businesses have imported over 32 GW of solar panels within two years, enhancing energy security at the household and industry levels. This surge is mostly driven by grassroot residential, commercial, and industrial roof-top installations instead of public sector funded or PPA-based large solar projects. High electricity costs (as in Bangladesh), unreliable electricity supply in the form of frequent blackouts, and desires for self-reliance are the root causes of the boom. Punjab—the largest province economically and in terms of population–accounts for 17.7 GW of solar capacity out of total solar capacity of 46.6 GW in the country in 2024. The result is phenomenal: reduction of electricity bill by up to 80% for Islamabad residents. Most of the power generation is still off-grid, although grid connected net-metered solar capacity also surged from 1.3 GW in early 2024 to 5.3 GW by April 2025. The country also imported 1.25 GWh equivalent of lithium battery packs in 2024. If this trend continues, total battery imports could reach 8.75 GWh by 2030, enough to meet over a quarter of peak demand, while solar could cover most of daytime electricity needs. By reducing dependence on imported fuels like LNG, this solar revolution is significantly reducing Pakistan’s BOP pressures. Pakistan’s solar revolution: from 0% to 25% in a decade. Solar is now Pakistan’s #1 electricity source. Not driven by government investment— driven by consumers.

Chinese overcapacity in manufacturing of solar power panels and the consequent sharp drop in solar panel costs have created an unique opportunity for solar revolution across the globe. In Pakistan, this favorable external development was also supported by duty free import of solar panels until 2024, which has now been increased to 10% from 2025. This unregulated expansion of solar power also created some problem for the public sector utilities in terms of grid load management and increased their financial loss in terms of capacity payments. Overall, Pakistan’s solar revolution and resulting problems associated with grid load management have important lessons to learn for Bangladesh.

3. Recent Developments on the Solar Power Front in Bangladesh

The import-dependent hydrocarbon lobby always discouraged the adoption of solar energy as an important source of power mix in Bangladesh despite publicly stated respectable national targets set for solar power. There are many narratives discouraging efforts towards realization of potential solar revolution in Bangladesh. The most important constraints in those narratives include (i) low sun exposure due to extended cloud cover during most of the rainy season; and (ii) scarcity of land in Bangladesh and the resulting potential conflict with agricultural land use and food security. Despite the apparent merits of these arguments, a closer review of the situation indicates that much of these arguments are not as relevant given that technological improvements made solar power quite cost effective in Bangladesh relative to any other modes of power generation. Despite limited solar exposure, industrial rooftop solar in Bangladesh costs less than TK 6 (US Cent 5) per kWh and utility scale solar costs around TK. 8-9 (US Cent 7-8), compared with the average grid lined average tariff of Tk 9-10 (US Cent 9-10) per kWh, even after blending cheap domestic gas with imported fuels. Certainly, compared with countries with dry sunny weather Bangladesh’s long-term marginal cost (LRMC) of solar power generation will be higher, but still it provides for economically most attractive return with lowest LRMC compared with other modes of power generation in Bangladesh.

Land issue deserves special consideration in Bangladesh, and efforts must be made to avoid multi-crop productive land for large scale solar parks. Through judicious and pragmatic land use Bangladesh has potential to realize huge volume of solar power across Bangladesh. Some of these are noted below:

• Rooftops of all large industries can be used for solar power. Many RMG owners and some industrial parks have already moved towards this direction and the potential is significant. The Government can conduct surveys and make it mandatory for all EPZ and SEZ authorities to ensure that all available rooftops and any other available space are fully utilized for solar power and banks can provide credit to the industries within the EPZs and SEZs or to the EPZ/SEZ authorities for solar power generation within a mandated short timeframe.

• All residential areas in major cities like Dhaka, Chottogram, etc. may be divided into several zones and contracted out to registered rooftop solar power producers under buy-back arrangement with BPDB and revenue sharing with homeowners. Each locality (say Gulshan or Dhanmondi) may be allocated to one rooftop produces based on a competitive process. In this way, millions of homes will come under solar power programs in a lightly regulated environment covering buyback terms and the minimum shares to the roof owners.

• Rooftop solar on all Government offices: The initiative undertaken during the Interim Government to install rooftop solar on most Government and public sector buildings aims to generate about 3,000-3,500 MW of power for adding to the national grid in addition to self-use. This initiative may also serve as a model for private companies/corporations to follow suit.

• Riverbanks, Chars/ shoals and other Water Bodies: There are thousands of kilometers of rivers crisscrossing all over Bangladesh. Solar panels can be erected along the banks of these rivers—which are primarily Khash (public) land–in a systematic and organized manner by devising appropriate policies to encourage the private sector. Teesta solar project is a good example of such initiatives and tens of thousands of MW worth of solar power can be generated along the rivers and southern coast lines of Bangladesh. Raised riverbeds or shoals are widely seen in many wide river systems and can be used for solar power projects along with certain types of fruits and vegetables. In a keynote paper prepared by an NGO named Change Initiative reports that only by utilizing 1% area of Kaptai Lake and the fish farms in coastal areas 3,000MW of electricity can be produced.

• Irrigation Pumps: Bangladesh currently uses 1.6 million pumps to irrigate the agricultural land. 80% of the pumps are still running on diesel requiring imported diesel. All these pumps can be converted to solar power, potentially generating 3,000-3,500MW of electricity during day time. In the boro plantation season (lasting about 4 months), the pumps may also run with power taken from the grid connection at night and during the remaining 8 months of the year the solar pumps should be able to supply power to the national grid based on net metering system. The initiative taken by IDCOL with support from development partners is a step in the right direction but needs to be scaled up significantly to have a noticeable impact on the economy.

• Tea gardens: There are 168 tea gardens in Bangladesh mostly in Sylhet, Moulovibazar, Habiganj, Chottogram areas with some on Banderban and Panchagarh. These tea estates in the country cover almost 280,000 acres of land, yielding about 2% of global tea production. Most of these tea planters are in financial distress due to lower prices and would like to place solar panels in the tea estates to generate solar power to augment their income and reduce power bill while not compromising on productivity in terms of tea output. Since all these tea estates are on publicly leased lands under certain strict land use conditions, the government policy in terms of land use would need to be reviewed for this investment by the tea estates to take place. In Bangladesh, generating one MW of solar typically requires approximately 3-4 acres of land for utility scale ground mounted projects. Given the enormous land mass under tea plantation, even if we assume that one third of the plantation area is covered by solar panels with high poles, and even if we assume 10 acres of plantation area to produce one MW of solar power, total power generation would amount to more than 9,300 MW. Generation of this much power would fundamentally change the financial prospects/viability of the tea economy in Bangladesh.

• Railways: Bangladesh Railways have a vast network of railway lines and wide swaths of land around the railway lines and stations and other facilities. Railways is the second largest owner of public land after the Ministry of Water Resources which manages all river banks.

A study by two NGOs—Coastal Livelihood and Environmental Action Network (CLEAN) and Bangladesh Environmental Lawyers Association (BELA)—titled “Myths &Reality about Land Availability for Solar Power in Bangladesh: Rangpur Division” finds that the eight districts of Rangpur Division have the potential to generate 11,944 MW of solar power even on the assumption that only 11% of the identified khas land in the division is utilized for solar power. This estimated generation capacity is more than 10 times the current peak hour demand in Rangpur division.

4. Policy Support Needed for Solar Revolution

Like every country, for a successful launching of renewable power revolution, Bangladesh government needs to implement the following key support measures:

• Like Pakistan and many other countries all import duties, VAT and Supplementary Duties on solar power related components like solar panels, inverters, and storage batteries should be completely abolished immediately. The same principle should also apply to wind turbines and related accessories.

• The Net Metering Policy should be expanded to all segments of households and businesses including removal of capacity limitations on individual rooftop solar systems to make investments attractive for businesses and households.

• Adopt policies for organized rooftop solar in urban areas and commercial power generation at various stable locations/land areas noted in Section 3. SREDA may be given the responsibility to divide major cities into several contiguous zones and auction out the contracts all rooftop solar zones to eligible private power producers through competitive bidding process.

• Each authority owning land usable for solar power generation, as mentioned and discusses above, should be given the responsibility for solar power development strategies in their respective areas in consultation with SREDA and IDCOL (if needed). SREDA should also establish annual targets for each of these land-owning authority for rapidly expanding solar power generation across Bangladesh without using productive agricultural farm land.

• Bangladesh Bank should also start low cost and longer-term financing to the investors by augmenting resources under the Green Transformation Fund (GTF). The Fund needs replenishment in terms of dollars/Euro for the renewable power program to expand rapidly. IDCOL, which offers concessionary loans to support irrigation and other solar projects, should expand its financing to cover more projects. IDCOL has started financing of some solar irrigation projects, but the scope of the program should be vastly expanded to replace the 1.3 million diesel run irrigation pumps by solar power systems to cut import bills during the boro crop season.

• Power purchases by the Bangladesh Power Development Board (BPDB) or Rural Electrification Board (REB) should allow some incentives in the form of higher unit prices for net purchases from the households and solar irrigation pumps to encourage rapid expansion of investment at the beginning by entrepreneurs. Experience of Germany and Pakistan clearly shows that such incentives really encourage the households towards adoption of solar rooftop or wind power at a rapid pace. Once the supply response is widely visible, the subsidy element may be reduced or eliminated over time.

Along with the supporting policy package, the government should make an institution like SREDA to oversee the implementation of the policy measures and also catalyze private investment in the solar power programs outlined above. An ambitious and transparent Monitoring and Evaluation (M&E) Framework needs to be developed to ensure implementation and hold the government agencies accountable for their failures in terms of planned implementation.

5. Starting an Electric Vehicle (EV) Revolution in Bangladesh

Bangladesh is seriously lagging in transforming its transportation system emission free (or reducing) green and electric. China is certainly the global leader on this front, significantly reducing demand for petroleum and natural gas in the country. As the world’s largest EV market, 54% of new car sales in the country in 2025 was EVs. China manufactured 12 million EVs in 2024, accounting for more than 70% of total global production. Despite some slowdown, EV sales continued to grow at a record pace of 1.3 million in the month of November 2025 alone. Driven by growing domestic demand, 60% of global EV sales took place in China so far.

EVs are also getting popular in Europe accounting for about 30% of global stock at the end of 2023. EVs are particularly popular in the Scandinavian countries and in the mainland Europe. Norway has the highest market penetration in per capita terms in the World, accounting for 117.3 car per 1000 people in 2021, followed by Iceland (69.3 per 1000) and Sweden (28.8 per 1000). Germany is leading the Europe in terms of the number of registered plug-in cars—[1.38 million] as of December 2021.

Bangladesh scenario is quite different and a mixed one. Until March 2025, the number of officially registered EVs—based on data from Bangladesh Road Transport Authority (BRTA)—was only 396, and another source placing the number growing to 515 by early 2026. Out of the March 2025 figure, most were motor cycles (243), with hardtop jeeps and private cars accounting for only 94 and 54 units, respectively. The situation has started to change with the introduction of brands like BYD leading in the four-wheeler segment (reportedly selling approximately 300 units in the first year).

The Government has set a target for 30% of all vehicles in the country to be EVs by 2030. However, Bangladesh’s four-wheeler market is still dominated by Japanese combustible engine reconditioned cars and SUVs—with strong reputation for reliability and tax incentives in favor of Japanese reconditioned vehicles (particularly Toyota). Extensive marketing networks and readily available parts and vehicle servicing has established the reconditioned Japanese cars in a firm footing. In contrast, only a few Chinese BYD, Cherry, Havel etc., are now operating in Dhaka with very limited nationwide dealership and service centers.

In the overall national interest, the Government should promote four-wheel EVs by reducing import duties of about 100% to something like 30%-50% in the next budget and provide incentives for manufacturing and assembling of four-wheeler EVs in Bangladesh. The absence of charging stations allowing rapid recharging of batteries is also a serious problem. As part of the nationwide network of charging stations, the government should instruct and incentivize the petrol pumps to install at least two charging points in each gasoline stations. These measures, if adopted expeditiously should help unleash an EV revolution in four wheelers in Bangladesh.

While the adoption of four-wheeler EVs has lagged behind, there has been a revolution in the adoption of 3-wheeler EVs all across Bangladesh. Driven by economic considerations—highly subsidized lifeline electricity tariff rates and cheap imports and domestic manufacturing—transportation system at the rural and urban areas across Bangladesh has been transformed to EVs. Millions of manual three wheelers—locally called Rickshaws—have been converted/modified to electricity-run vehicles over the last 5-10 years. Initially these 3-wheeler EVs were banned from cities, major roads and highways, but over time such bans have become ineffective and ignored and about 4-6 million 3-wheeler EVs are now plying all over Bangladesh, providing clean/green and faster transportation to about 120 million people every day.

The transformation that has happened in 3-wheeler EVs is massive and not reversible. What the government needs to do is to regulate this market through proper licensing, training of 3-wheeler EV drivers regarding traffic rules and issuing them licenses after completion of successful training and driving tests, and enforcing the traffic rules and regulations forcefully. The license fees could be important source of revenues for the local government authorities. The massive training programs would help improve flow of traffic and reduce number of serious accidents both of which are serious problems contributing to unnecessary delays in urban areas and frequent fatal accidents involving the 3-wheelers.

6. Concluding Observations

Green/renewable energy have gained a lot of momentum in recent years due to growing awareness about climate change and also supported by technological innovations making renewable energy a very competitive and cost-effective way to generate power. Economies across the globe have been moving to green and renewable energy, albeit at uneven paces. Some countries like China, Scandinavian and other European countries became global leaders, while some countries which are self-sufficient or exporters of fossil fuels like OPEC Plus (including GCC), the USA, Australia were actively working against the global movement to fight climate change. In some countries like Bangladesh import dependent fossil fuel lobby was very active and executed an import dependent fossil fuel-based power development strategy over the last one and half decade.

Under pressure from international and national climate activists including commitments under the various COPs, the government set some targets like generating 20% of power from renewable sources by 2025 and further to 40% by 2040. But in reality, due to strong fossil fuel lobby, government policies and political commitments were not really supporting the realization of these objectives and renewable energy almost always remained an afterthought. While our neighbors like India and Pakistan succeeded in bringing about solar power revolutions, Bangladesh was deprived of the benefits from cheap homegrown solar power and is now most exposed in terms of energy security due. The Middle East war has clearly demonstrated that Bangladesh’s energy and national security clearly depends on our energy self-reliance, which is possible largely through a revolution in solar power. As shown above, it is a myth–deliberately orchestrated by the fossil fuel lobby–that Bangladesh does not have enough land for solar power. It is our expectation that the new government does not fall for the same powerful international and national fossil fuel lobby and misses the historic opportunity to rectify the past mistakes and avoid the associated economic costs.

The government needs to develop a detailed solar power development roadmap focusing on all the key areas identified above and establish specific targets for each of these areas. Give the expected growth in domestic demand for power and taking into account the rapidly declining trend in stock of proven and usable natural gas reserves and the daily volume of domestic supply of natural gas, a surge in solar power is likely to be the best way out for supporting the economy with necessary electricity supply at affordable cost. All indications point to the growing interest of the industry and IPPs for boosting solar power supply in Bangladesh. The strategy outlined above would need to be supported by a package of policy measures (noted above) to encourage households, industrial rooftop solar projects, and also support companies establishing solar projects on khash lands, river banks and river beds, railway lands etc. The strategy/roadmap for renewable power in Bangladesh may be jointly sponsored by SREDA and the Power Division, with active involvement of all relevant stakeholders. Bangladesh power sector has already fallen behind and the domestic industries and households have been suffering for a long time. Thus, immediate steps are needed to rectify the past mistakes, implement appropriate course correction, and usher a revolution in the renewable power front starting with the new budget to be announced in early June 2026.